2026/03/04 | Diego Ciongo & Soledad Castagna

At this monetary policy meeting, the central bank’s Monetary Policy Committee (MPC) cut the policy rate by 75-bps to 5.75%. The decision aligns with our call, while the market expected a 50-bps cut (as per Bloomberg and central bank survey). The easing cycle has accumulated 350 bps since July.

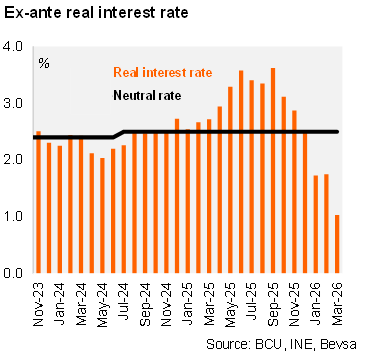

The inflation outlook is under control and economic activity is weak. The BCU highlighted that inflation and inflation expectations remain under control, while activity leading indicators surprised to the downside. In fact, economic activity entered in technical recession in 4Q25 according to the central bank monthly GDP proxy. The BCU is consolidating its expansionary stance. Average inflation expectations for the monetary policy horizon (24 months) stand at 4.67% (down from 4.79% in the previous meeting), within the tolerance range for the ninth consecutive month. Consequently, we estimate the ex-ante real policy rate at 1.04%, below the BCU’s neutral real rate estimate of 2.5%.

Regarding the external front, the communiqué highlighted the recent increase in oil prices amid the US-Iran conflict and its potential impact on inflation. The MPC mentioned that inflation risks seem more balanced than in previous meetings. However, the BCU also mentioned that the main risk is inflation remaining below the target during the monetary policy horizon.

Our take: Our terminal rate forecast stands at 5.50% for YE26, assuming one more additional cut in the next meeting scheduled for 21 April. However, recent pressures on oil prices amid the US and Iran conflict could lead to a pause in the easing cycle. The minutes of today’s meeting will be published on March 10.