2026/03/24 | Diego Ciongo & Soledad Castagna

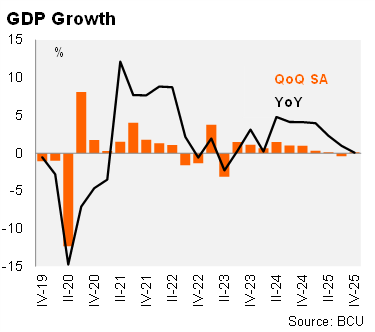

GDP grew 0.1% YoY in 4Q25, down from 1.0% YoY in 3Q25. At the margin, using the central bank’s seasonally adjusted series, GDP increased 0.1% QoQ/sa in 4Q25 – outperforming the monthly GDP proxy, which had pointed to a 0.6% QoQ/sa contraction. For the full year, GDP expanded 1.8% in 2025, below the 3.3% growth recorded in 2024.

Mixed performance across sectors. On the supply side, annual growth was mainly supported by financial services (+4.0% YoY), manufacturing (+1.7% YoY), and commerce (+1.2% YoY), the latter boosted by higher sales of clothing and pharmaceuticals. Tourism related services remained broadly unchanged compared to 4Q24. Conversely, the primary sector contracted 7.7% YoY in 4Q25 due to a weaker soybean harvest amid drought conditions, while the energy sector declined 5.4% YoY given lower electricity generation.

Domestic demand strengthened in 4Q25. Domestic demand (excluding inventories) rose 1.5% YoY in 4Q25, unchanged from 3Q25. This was driven by a 2.0% YoY increase in consumption—supported by private consumption (+1.9% YoY) and a 2.2% YoY rise in public spending. Gross capital formation increased 2.2% YoY, largely reflecting higher inventories, particularly in oil, vehicles, and cellulose. External demand softened: exports of goods and services fell 1.9% YoY (vs. +5.2% YoY in 3Q25), pressured by weaker sales of vehicles, cellulose, and electricity, partly offset by higher tourism revenues. Imports rose 5.1% YoY (vs. +4.6% YoY in 3Q25), driven by consumer goods and greater outbound tourism spending.

Our take: Our 2026 GDP growth forecast stands at 1.5%, but now with downside risks stemming from a weak statistical carryover (-0.1%), softer early year leading indicators, and the likelihood of the drought impacting the soybean harvest.