2026/05/05 | Diego Ciongo & Soledad Castagna

Inflation rose by 0.54% MoM in April (from +0.32% a year ago and a 5-year median of 0.54%), in line with our call and the BCU’s survey median, both at 0.6% MoM. The main upward contribution came from Transport, which rose 2.98% MoM (+0.31 p.p. incidence), driven by a 7% MoM increase in oil prices and a sharp rise in airfare prices (+17.94% MoM). Clothing prices also increased (+1.88% MoM; +0.04 p.p.), as did Housing, water, electricity, gas and other fuels (+0.66% MoM; +0.09 p.p.). On the downside, Recreation, sports and culture declined 0.23% MoM, while vegetable prices fell 0.63% MoM and fruit prices dropped sharply (-5.40% MoM), partially offsetting the headline increase.

Core inflation (CPI‑CE VFC), which excludes fruits & vegetables and fuel prices, rose by 0.35% MoM, matching the increase recorded in April 2025. Meanwhile, the CPI‑CE VFCTA—excluding nearly 26% of the headline basket (fruits and vegetables, fuels, and centrally priced or administered items) posted a 0.42% MoM gain, broadly in line with the 0.43% MoM increase observed in the same month last year. Importantly, the National Statistical Institute includes new measures in the report thus the Tradable CPI rose by 0.48% MoM while the non-tradable CPI rose by 0.35% MoM.

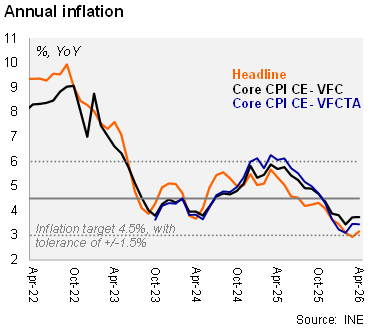

On a year‑over‑year basis, all CPI measures remain within the BCU’s of the 4.5% target’s +/-1.5% tolerance range. Headline inflation rose to 3.16% YoY in April, up from 2.94% in March. Core inflation, however, remained broadly stable at 3.74% YoY (from 3.73% in the previous month), while CPI‑CE VFCTA edged slightly lower to 3.45% YoY, from 3.47% in March, reinforcing signs of contained underlying inflation pressures. Moreover, tradable CPI rose by 1.28 % YoY, reflecting the strong peso over the last year while the non- tradable increased 5.86% YoY in April.

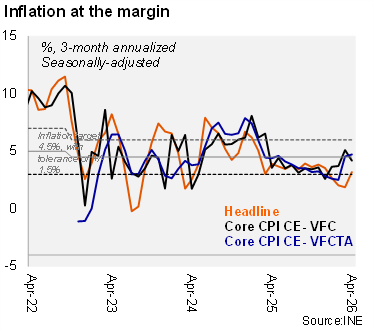

At the margin, headline inflation shows an acceleration, while core inflation pressures ease. Based on our seasonally adjusted estimates, three‑month annualized headline inflation increased to 3.2% in April, up from 1.9% in March. In contrast, core inflation decelerated to 4.2%, from 5.1% previously. Meanwhile, the CPI‑CE VFCTA edged slightly higher to 4.7%, from 4.6% in the prior month.

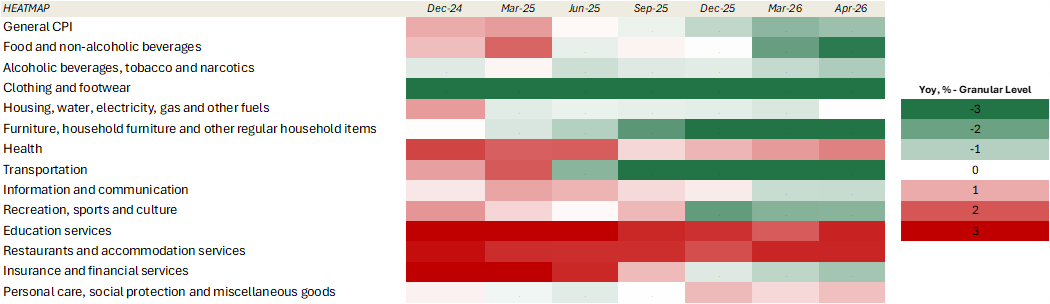

Our CPI heatmap shows that 62% of selected items are below the central bank’s target (4.5%), below the previous month (69%), but above the April 2025 figures (38%).

Our Take: Our YE26 inflation forecast stands at 4.9%, driven by recent global developments, particularly the impact of higher oil prices on consumer basket components and their indirect, lagged effects on inflation. May’s CPI will be released on June 3. On the monetary front, we expect the policy rate to remain unchanged at 5.75% through 2026, as the Central Bank balances inflation risks against still‑moderate domestic activity. Nonetheless, a rate hike cannot be ruled out, contingent on the extent of oil price pass‑through to headline inflation and, more importantly, to inflation expectations.