2026/04/22 | Diego Ciongo & Soledad Castagna

In the recent monetary policy meeting, the Central Bank of Uruguay (BCU) decided to keep the policy rate on hold at 5.75%. The decision was fully in line with our expectations and market consensus, reflecting the sharp increase in global uncertainty following the escalation of the Middle East conflict, which has pushed energy prices significantly higher. This pause comes after a cumulative easing of 350 bps since July 2025.

The domestic macro backdrop remains supportive. The inflation outlook continues to be benign, while economic activity shows clear signs of improvement in 1Q26. The BCU reiterated that both headline inflation and inflation expectations remain well contained. Leading activity indicators point to stronger momentum at the start of 2026, underpinned by a recovery in private consumption.

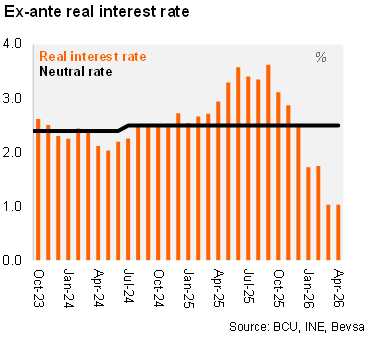

Inflation expectations remain firmly anchored around the target across the policy horizon, despite the prolonged geopolitical tensions. Analysts and financial markets continue to forecast annual inflation at 4.5%, while firms’ expectations remain stable at 5%. Average inflation expectations over the 24‑month horizon stand at 4.67%, unchanged from the previous meeting and within the tolerance band for the tenth consecutive month. Against this backdrop, we estimate the ex‑ante real policy rate at 1.04%, still well below the BCU’s neutral real rate estimate of 2.5%, indicating that the monetary stance remains accommodative.

On the external front, the communiqué emphasized an exceptionally uncertain global environment, characterized by elevated volatility in currency and commodity markets. Oil prices remain well above pre‑conflict levels, while higher logistics costs are adding to global inflationary pressures. The MPC stressed that the materialization of these external inflation risks will depend on both the duration and intensity of the conflict, as well as the broader adjustment of key macroeconomic variables. In this context, monetary policy—backed by anchored inflation expectations and headline inflation at the lower bound of the tolerance range—is well positioned to absorb potential external shocks.

Our view: We expect the policy rate to remain on hold at 5.75% throughout the rest of 2026. Looking ahead to 2027, we anticipate the beginning of a gradual tightening cycle, as global conditions normalize and domestic activity gains traction, generating firmer demand‑side pressures. That said, a rate hike in 2026 cannot be ruled out, depending on the pass‑through from higher oil prices to inflation and, more importantly, to inflation expectations. The minutes of today’s meeting are scheduled for publication on April 24.