2026/05/26 | Diego Ciongo & Soledad Castagna

At today’s monetary policy meeting, the Central Bank of Uruguay (BCU) unanimously decided to keep the policy rate on hold at 5.75%, for the second consecutive month. The decision was fully in line with our expectations and market consensus.

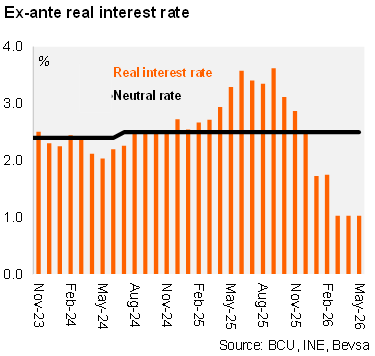

Inflation and inflation expectations remain aligned the BCU’s target (4.5%). Average inflation expectations over the 24- month horizon stand at 4.67%, unchanged from the previous meeting and within the tolerance band for the thirteen consecutive months. Against this backdrop, we estimate the ex ante real policy rate at 1.04%, still well below the BCU’s neutral real rate estimate of 2.5%, indicating that the monetary stance remains accommodative. On activity, the BCU highlighted a recovery in 1Q26, but the outlook for the rest of the year points to moderate growth.

Deterioration of the external backdrop. The ongoing conflict in the Middle East is keeping energy prices high amid volatility and inflationary pressures. In addition, long-term interest rates are rising, creating a less favorable financial environment for emerging economies. Thus, the Copom concluded that the balance of risks to inflation had shifted slightly upward due to oil prices remaining at higher levels than anticipated at the previous meeting.

Our view: We expect the policy rate to remain on hold at 5.75% throughout 2026, as the Central Bank continues to balance rising inflation risks against still‑moderate economic activity. However, the recent oil price shock introduces an asymmetric risk profile: while a near‑term hike is not our base case, a tightening bias cannot be ruled out in 2026 if higher fuel costs translate into a stronger‑than‑expected pass‑through to headline inflation and, more importantly, begin to affect medium‑term inflation expectations. The next monetary policy meeting is scheduled for July 1.