2026/03/04 | Diego Ciongo & Soledad Castagna

Inflation rose by 0.35% MoM in February (from +0.69% a year ago and a 5-year median of 0.93%), well below our call and the BCU’s survey median, both at 0.6% MoM. The main monthly impact came from housing, electricity and water which rose by 1.52% MoM (incidence of 0.20 p.p.), given the reversal of the temporary energy discount in December and January. Moreover, furniture, household goods and other regular household items rose by 1.20% MoM (incidence 0.06 p.p) and personal care, social protection and miscellaneous goods increase by 0.83% MoM (incidence of 0.04 p.p.). On the other hand, recreation, sports and culture prices fell by 0.95% MoM (incidence of -0.05 p.p.), clothing prices decreased by 1.60% MoM (incidence of -0.03 p.p.) due to the liquidation of the spring-summer season, and food and non-alcoholic beverages prices decline of 0.06% MoM (incidence -0.02 p.p.) due to lower fruits and meat prices.

Core inflation (CPI CE VFC) (excluding fruits & vegetables and fuel prices) increased 0.36% MoM, from 0.72% MoM in February 2025. The CPI-CE VFCTA, which excludes almost 26% of the general basket (fruits and vegetables, fuels, and centrally priced or administered products) rose by 0.16% MoM, from 0.28% MoM in the same month one year ago.

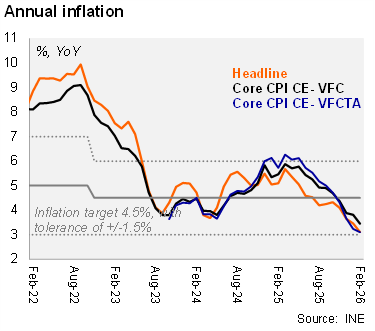

On an annual basis, all CPI readings drifted towards the floor of the 4.5% target’s +/-1.5% tolerance range. Headline inflation fell to 3.11% YoY in February from 3.46% in January, marking its lowest historical print. On the other hand, the core reading decreased to 3.45% from 3.82% in the previous month, while the CPI-CE VFCTA fell to 3.10% YoY, from 3.23% YoY in January.

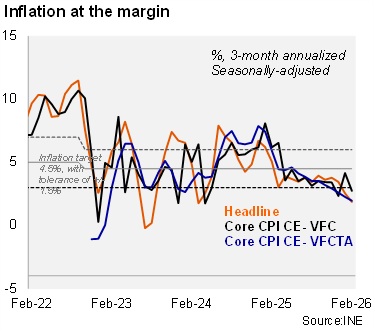

At the margin, headline and core inflation decelerate. Using our seasonally adjusted figures, the three-month annualized headline inflation fell to 1.9% in February (from 2.5% in January), while core inflation fell to 2.7% from 4.2% before. Finally, the CPI-CE VFCTA reading fell to 2.0%, from 2.3% in the previous month.

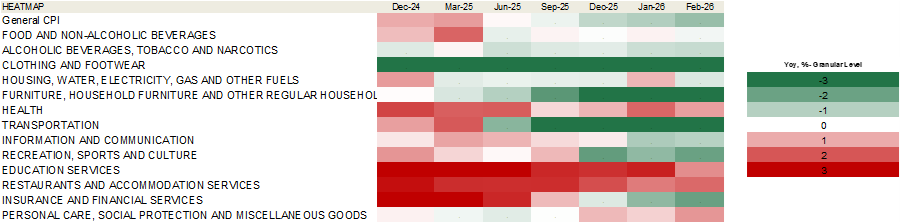

Our CPI heatmap shows that 69% of selected items are below the central bank’s target (4.5%), above the previous month (54%) and February 2025 figures (54%).

Our Take: Our inflation forecast for YE26 stands at 4.5%, in line with the central bank's target, implying a rebound later in the year. March’s CPI will be released on April 2. Our terminal rate forecast stands at 5.50% for YE26, assuming one more additional cut in the next meeting scheduled for 21 April. However, recent pressures on oil prices amid the US and Iran conflict could lead to a pause in the easing cycle.