2026/05/15 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

Peru’s monthly GDP proxy expanded 3.21% YoY in March, above both the Bloomberg median (2.4%) and our 3.0% forecast, reinforcing the narrative of solid macro resilience at the start of the year. Growth was led by construction, commerce, manufacturing, and services, which more than offset the impact from a two‑week domestic natural gas shortage.

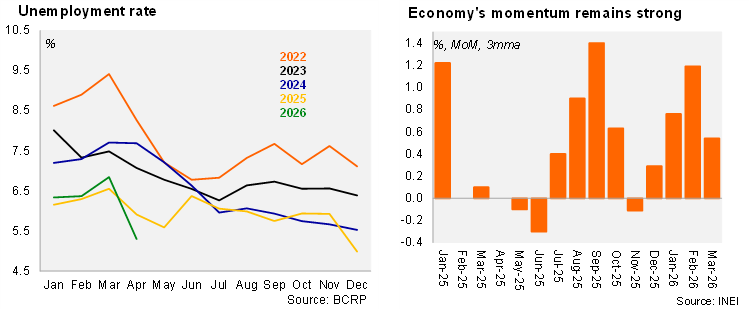

On a sequential basis, activity edged down slightly by 0.05% m/m (seasonally adjusted, INEI series), following a strong run in previous months, suggesting some normalization after a robust start to the year.

The March print confirms that activity expanded 0.5% QoQ (SA) in 1Q26, while full‑year 2026 carryover reaches 1.4%, providing a constructive base for annual growth dynamics.

Labor market data continues to confirm the strength of domestic demand. Metropolitan Lima unemployment (3MMA) declined to 5.3% in the rolling quarter to April (from 6.8%), while employment rose 6.1% YoY, with ~335k jobs created over the past 12 months.

Our Take: High-frequency indicators, including capital goods imports and cement dispatches, point to ongoing investment momentum and resilient private consumption, consistent with the recent upside surprise in activity. We maintain our 2026 GDP growth forecast at 3.1%. Elevated global uncertainty and weather-related risks tied to a potential El Niño may weigh on economic activity. The GDP for 1Q26 should be published at the end of the month while April activity data will be released on June 15.