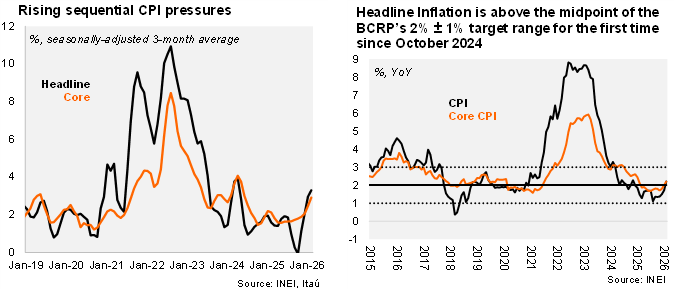

Consumer prices rose by 0.69% from January to February, significantly above the Bloomberg median and the historical average of 0.17%. The main driver was food & non‑alcoholic beverages (2.0%; 48bp contribution), due to supply disruptions in sweet peas (106%) and chicken (8.5%). Housing, water, electricity & household fuels also contributed significantly (1.0%; 9bp contribution), following a 10% increase in water supply tariffs (14bp contribution). Restaurants & hotels (0.3%; 5bp contribution) and transport (0.3%; 4bp contribution), driven by higher airfares (2.1%), also added to the headline reading.

Core inflation, which excludes volatile food and energy components, was more favorable, rising 0.36% MoM.

On an annual basis, headline inflation increased by 51bp to 2.21%, rising above the midpoint of the central bank’s 2% ± 1% target range for the first time since October 2024. Core ex‑food & energy inflation rose 20bp to 2.2% YoY. Sequential price pressures are rising: headline inflation reached 3.3% QoQ/SAAR, up from 2% in 4Q25, while core inflation rose to 2.9% QoQ/SAAR.

Our take: We expect some statistical payback in March. Our year‑end inflation forecast of 2% faces upside risks amid rising geopolitical tensions and potential pressures on oil prices. Also, the Coastal El Niño phenomenon poses inflation risks in the coming months. We expect the BCRP to keep the policy rate at 4.25% at next week’s meeting, likely adopting a more cautious tone given the closed output gap, the timing of upcoming FOMC cuts, and increasing domestic political uncertainty ahead of the April 12 general elections.