2026/04/10 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

At its April Monetary Policy Meeting, the Central Bank of Peru (BCRP) kept its benchmark interest rate unchanged at 4.25% for a seventh consecutive month, in line with broad market expectations. The Board reiterated that the recent increase in inflation observed over the past two months has been mainly driven by transitory global and domestic supply shocks, which are expected to fade in the coming months.

While forward guidance remains explicitly data-dependent, the BCRP introduced a subtle shift in its communication. The Board noted that upcoming policy decisions will also consider the expected persistence of supply-side shocks—an element that was not explicitly highlighted in the previous statement.

The assessment of the external environment remained cautious, reflecting heightened global risks stemming from geopolitical tensions in the Middle East, ongoing global energy shocks, and increased financial market volatility. That said, the global growth outlook remains positive, and Peru’s terms of trade continue to be favorable.

Regarding the domestic scenario, the communiqué acknowledged that both headline and core inflation are expected to re-enter the 1-3% target range by year-end and converge toward the midpoint only by 2027, as current supply shocks dissipate. This represents a more cautious inflation trajectory than in the previous guidance, which anticipated inflation fluctuating around the midpoint over the policy horizon. The BCRP also reiterated that economic activity remains close to its potential level.

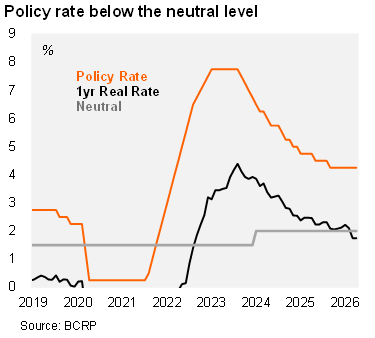

The BCRP’s Economic Expectations Survey, published today, showed that 12‑month-ahead inflation expectations rose to 2.5% in March, placing the ex‑ante real policy rate at 1.75%, below the estimated neutral rate of 2.0%. Analysts revised their 2026 GDP growth forecast down from 3.2% to 2.9%.

Our take: Our baseline scenario points to the policy rate remaining at 4.25% in the near term, alongside a cautious policy stance. However, amid rising inflationary pressures and still‑favorable terms of trade, the balance of risks is increasingly tilted toward a potential rate hike. The next Monetary Policy Meeting is scheduled for May 14.