2026/02/13 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

At its February monthly monetary policy meeting, the Central Bank of Peru (BCRP) kept the benchmark interest rate at 4.25% for the fifth consecutive month, in line with broad market expectations. Forward guidance remained unchanged and data‑dependent. Notably, the statement once again omitted the reference indicating that the policy rate was very close to the estimated real neutral level.

The main change in the communiqué was its assessment of the external environment, highlighting stronger‑than‑expected global growth and the country’s “exceptionally favorable terms of trade,” both of which, in our view, reduce the urgency to lower the policy rate again to our terminal rate of 4.0% (the BCRP’s nominal neutral rate).

The statement’s assessment of domestic conditions remained virtually unchanged. The BCRP reiterated its positive inflation outlook (with headline inflation expected to return to the 2% target midpoint) and stated that economic activity is close to potential, with most business sentiment indicators still in positive territory.

Of note, as has been the case since reserve purchases began in November, the statement again omitted references to spot dollar purchases that have reached USD 3.2 billion since the last meeting, and a cumulative somewhat above USD6 billion since November.

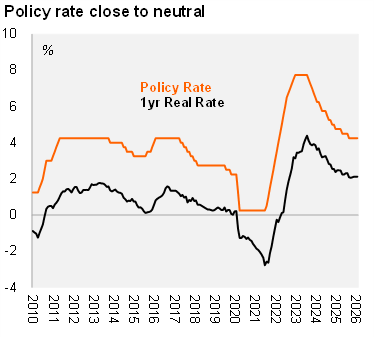

Our take: We expect the BCRP to bring the policy rate down to the 4% neutral level in the coming months. The Central Bank’s policy stance is currently near neutral, with the ex‑ante real rate standing at 2.2%, only slightly above the estimated real neutral rate of 2.0%. With the output gap largely closed and inflation expectations anchored, there is limited need to push monetary policy into expansionary territory. The next monetary policy meeting is scheduled for March 12.