2026/05/15 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

At its May Monetary Policy Meeting, the BCRP kept its benchmark rate unchanged at 4.25% for the eighth consecutive meeting, in line with our call and consensus. Forward guidance remains explicitly data-dependent, noting that the Board will closely monitor incoming information on inflation and its determinants.

The assessment of the external backdrop remains cautious, reflecting elevated global risks stemming from geopolitical tensions in the Middle East, ongoing energy market disruptions, and heightened financial volatility. That said, the global growth outlook remains broadly supportive, while Peru’s terms of trade continue to be favorable.

On the domestic front, the communiqué expects both headline and core inflation to return to the target range by year-end and to converge toward the 2% midpoint by 2027. The current inflation spikes are attributed to energy price shocks, fuel supply disruptions, and adverse weather conditions and BCRP expects that it will fade.

Regarding activity, domestic demand is now described as strengthening, with the economy potentially operating above potential (the BCRP removed the previous reference to activity being around potential).

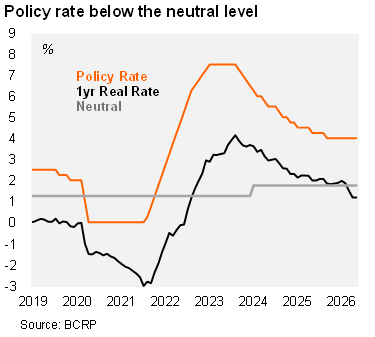

Overall, the real policy rate is estimated at around 1.75%, still below the BCRP’s neutral real rate of approximately 2.0%.

Our take: The BCRP has clearly adopted a wait-and-see approach in recent meetings. Our baseline scenario has the policy rate remaining at 4.25% in the near term, alongside a cautious policy stance. However, amid rising inflationary pressures — including the Middle East conflict and potential El Niño impacts — and still-strong terms of trade, the balance of risks is increasingly skewed toward a potential rate hike. The next Monetary Policy Meeting is scheduled for June 11.