2026/05/04 | Andrés Pérez M., Vittorio Peretti, Andrea Tellechea & Ignacio Martínez

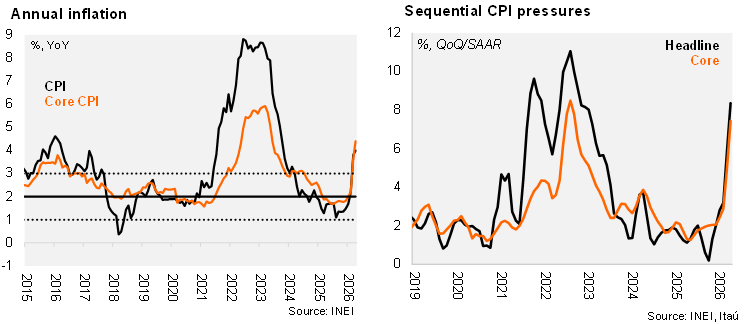

Consumer prices in Lima rose by 0.52% from March to April (0.32% in April last year), lifted by a 3.4% rise (+45bps) in the transportation division, as higher global oil prices get passed on to consumers. The print was well above the Bloomberg median (0.22%) and our call (0.24%). Higher prices in restaurants were another key upside pull, alongside a tariff adjustment to electricity prices. The food and beverage division declined 0.3% MoM, dragged by meat prices. On an annual basis, headline inflation increased by 21 bps to 4.01% YoY, well above the 2% ± 1% target range. Core inflation excluding food and energy sits at 4.41%.

Sequential inflation pressures surge. Headline inflation reached a sizable 8.4% QoQ (SAAR) in the rolling quarter, up sharply from 2.0% in 4Q25, while core inflation climbed to 7.4% QoQ (SAAR), also well above the 2.1% recorded in the previous quarter.

Our take: Our year-end inflation forecast sits at 2.8%, with upside risks. For 2027, we continue to expect inflation to gradually converge toward the midpoint of the target range, as supply-side pressures fade. The BCRP’s well-deserved credibility should help keep medium-term inflation expectations anchored and bring about disinflation. With the policy rate at 4.25%, slightly above the BCRP’s estimated neutral rate of around 4%, amid rising inflationary pressures and still-favorable external conditions, the balance of risks appear increasingly tilted toward a potential rate hike.