2026/03/27 | Diego Ciongo & Soledad Castagna

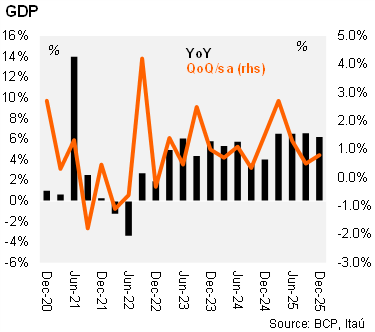

Paraguay’s GDP expanded by a robust 6.6% in 2025. In 4Q25, activity grew 6.2% YoY, easing slightly from 6.7% in 3Q25. From a supply-side perspective, all sectors posted positive growth during the quarter. The annual outcome was largely driven by strong performances in agriculture (20.8% YoY) and electricity generation (13.2% YoY), reflecting higher water levels in the Paraná River. Services increased by 5.7% YoY, construction by 4.3%, livestock by 3.9% and manufacturing by 3.7% YoY. As a result, full-year GDP growth accelerated from 4.7% in 2024 to a solid 6.6% in 2025. On a sequential basis, seasonally adjusted GDP rose 0.8% QoQ in 4Q25, implying a statistical carryover of 1.2% for 2026.

Domestic demand strengthened towards year-end. Internal demand rose by 7.0% YoY in 4Q25, up from 6.3% in 3Q25, mainly supported by consumption. Total consumption expanded by 4.3% YoY, with private consumption increasing 5.7% while public consumption contracted 2.6%. Gross fixed capital formation grew by a more moderate 1.3% YoY, decelerating sharply from 13.2% in 3Q25, largely driven by investment in construction. On the external front, exports of goods and services increased by 1.4% YoY, down from 10.3% in the previous quarter, reflecting lower soybean and corn exports. Imports rose by 3.3% YoY (from 8.9% in 3Q25), led by higher purchases of machinery and equipment as well as chemical products.

Our take: We maintain our 2025 GDP growth forecast at 4.0%, underpinned by a favorable statistical carryover and the outlook for a stronger soybean harvest. From the demand side, we expect private consumption to remain a key growth driver, supported by positive spillovers from Argentina. The Middle East conflict, however, represents a negative risk to economic activity given the country’s status as a net oil importer. Higher domestic fuel prices would likely weigh on consumption and internal demand, while a larger oil import bill would pressure the external accounts, particularly if elevated prices persist.