2026/05/04 | Diego Ciongo & Soledad Castagna

CPI increased 0.8% MoM in April, exceeding our call and the market consensus (both at 0.6%). The upside surprise was largely driven by a sharp adjustment in fuel prices (+12.1% MoM). These pressures were partially offset by durable goods (-0.1% MoM), reflecting the disinflationary impact of a strong PYG, and food prices (-0.1% MoM), driven primarily by fruits and vegetables, which declined 0.3% MoM. Importantly, core CPI X1 (excluding fruits and vegetables, regulated services and fuels) fell by 0.1% MoM, a sharp deceleration from 0.7% MoM a year earlier.

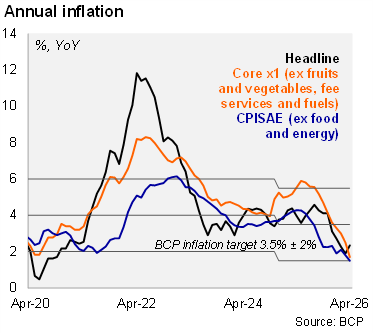

On an annual basis, headline inflation accelerated to 2.3% YoY in April, up from 1.9% in March, reflecting the fuel shock, while core X1 inflation eased to 1.7% YoY, down from 2.5% the previous month. Both headline and core remain comfortably within the tolerance range of the BCP’s inflation target (3.5% ±2%), underscoring the strength and credibility of the disinflation process. Consistently, the core ex food and energy inflation (CPISAE) fell to 1.5%, from 1.8%, approaching the lower bound of the target’s tolerance range.

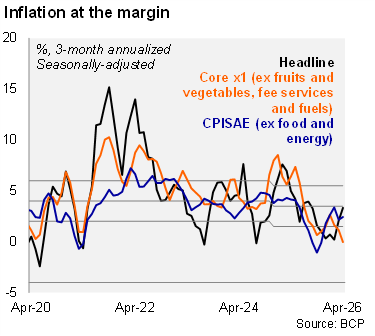

Momentum indicators remain mixed at the margin. On a seasonally adjusted basis, three‑month annualized headline inflation jumped to 3.3% (from 2.1% in March), fully reflecting the fuel-driven shock, while core inflation momentum softened sharply to 0.0%, from 1.2%, highlighting the absence of generalized price pressures.

Our take: We see upside risks to our 3.5% YE26 inflation forecast. The string of upside surprises, combined with a new fuel price increase effective in May, tilts risks to the upside in the near term. That said, muted core inflation dynamics should allow the BCP to remain patient, and we continue to expect the policy rate to stay on hold at 5.5% throughout 2026. The May CPI print will be released on June 2.