2026/04/06 | Diego Ciongo & Soledad Castagna

CPI increased 0.8% MoM in March, exceeding both our call (0.6%) and the market consensus (0.4%). The upside surprise was largely driven by a sharp adjustment in fuel prices (+9.8% MoM), which contributed 0.6 p.p. to the monthly print. Food prices increased 0.6% MoM, driven primarily by fruits and vegetables, which surged 4.5% MoM and contributed 0.2 p.p. to headline inflation. Service prices posted a modest 0.1% MoM increase. These pressures were partially offset by durable goods (-0.6% MoM), reflecting the disinflationary impact of a strong PYG. Importantly, core CPI X1 (excluding fruits and vegetables, regulated services and fuels) remained flat at 0.0% MoM, a sharp deceleration from 0.5% MoM a year earlier, reinforcing the view that underlying inflation pressures remain contained.

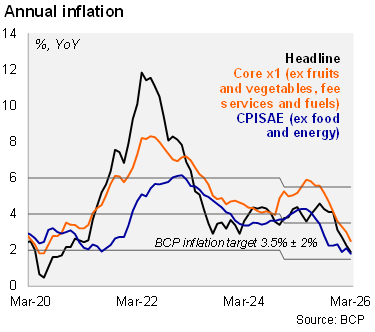

On an annual basis, headline inflation decelerated to 1.9% YoY in March, down from 2.3% in February, while core X1 inflation eased to 2.5% YoY, from 3.0% the previous month. Both measures continue to sit comfortably within the BCP’s target band (3.5% ±2%), underscoring the credibility of the disinflation process.

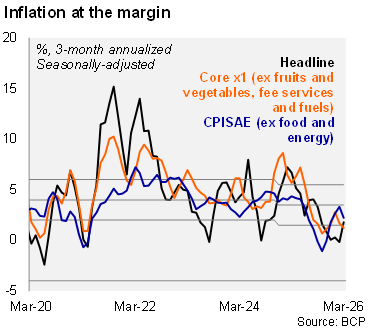

Momentum indicators remain mixed at the margin. Seasonally adjusted estimates show that three-month annualized headline inflation rebounded to 1.8% (from -0.2% in February), reflecting the fuel-driven shock, while core inflation softened further to 1.2% (from 1.7%), pointing to easing domestic demand-side pressures.

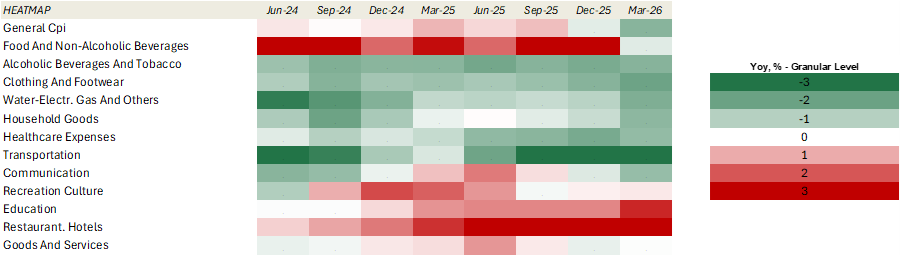

Our heat map shows that 75% of CPI items are currently running below the central bank’s 3.5% target, up from 67% in the previous month and 50% in March 2025, underscoring the increasingly broad-based nature of the disinflation process.

Our take: We continue to expect inflation to close the year at 3.5%, broadly in line with the BCP’s target. Upside risks remain skewed higher due to elevated oil prices and their likely pass‑through to domestic inflation. That said, recent benign core inflation dynamics support our baseline call. As a result, we maintain our view that the policy rate will remain on hold at 5.5% throughout this year . April’s CPI will be released on May 4.