2026/04/22 | Diego Ciongo & Soledad Castagna

In the recent monetary policy meeting, the BCP unanimously decided to leave the policy rate unchanged at 5.50%, maintaining a neutral monetary policy stance. The decision, which was in line with our expectations and market consensus, reflects the persistence of elevated uncertainty linked to geopolitical tensions in the Middle East, which have recently triggered a sharp rise in energy prices.

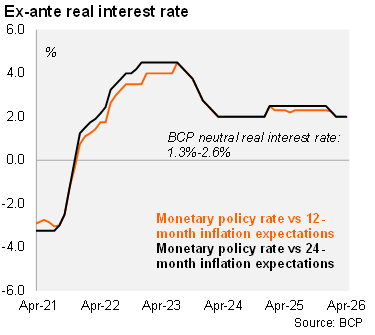

The Committee noted that short‑term activity indicators continue to point to a solid expansion of economic activity during the first months of the year. Consistent with this outlook, the latest Monetary Policy Report (MPR) maintained the 2026 GDP growth forecast at 4.2%. On the inflation front, the 2026 projection was also left unchanged at 3.5% in the MPR. While fuel prices have risen more sharply than anticipated in December, inflation dynamics across the remainder of the consumption basket have been more benign than expected during the first quarter. This offset has so far allowed the end‑year inflation forecast to be upheld. Importantly, under the baseline scenario, the Committee assumes that the recent energy‑price shocks are transitory, implying a contained and temporary pass‑through to headline inflation. Following today’s decision, we estimate the one‑year ex‑ante real policy rate remains at 2.0%, placing it comfortably within the BCP’s estimated neutral real rate range of 1.3%–2.6%.

Our view: We expect the policy rate to remain on hold at 5.50% throughout the remainder of 2026. However, upside risks dominate, driven by firmer Brent prices and their likely pass-through to inflation. That said, benign core inflation dynamics validate our baseline scenario. The next monetary policy meeting is scheduled for May 22.