2026/03/04 | Diego Ciongo & Soledad Castagna

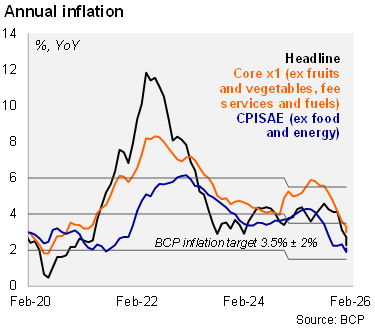

CPI remained flat in February (0.0% MoM), below our forecast (0.1%) and below the market median (0.3%). Service prices increased (1.1% MoM), mainly reflecting the rise in education services (5.8% MoM). Nonetheless, monthly declines in food goods (-0.8% MoM) and fuel (-2.7% MoM), supported by strong PYG, helped contain the monthly uptick. Core CPI x1 (excludes fruits and vegetables, regulated service prices and fuel) stood at 0.1% MoM (from 0.4% a year ago). On an annual basis, headline inflation fell to 2.3% in February, the lowest annual print since December 2020, while core X1 CPI decreased to 3.0%, from 3.3% in the previous month. We note that both the headline and the core remain within the tolerance band of the BCP’s inflation target (3.5% +/- 2%).

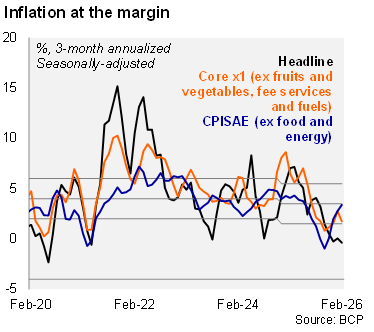

At the margin, headline and core inflation decelerate. Using our seasonally adjusted estimates, the three-month annualized headline inflation reading fell to -0.4% in February (from 0.1% in January), while core inflation fell to 1.7% (from 2.8% in the previous month).

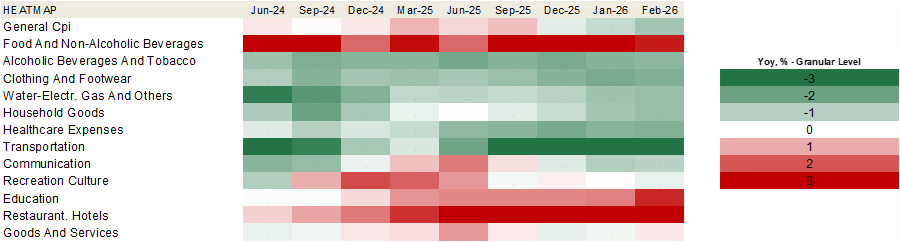

Our heat map shows that 67% of the items are below the central bank's 3.5% inflation target, unchanged from the previous month's figure, but above February 2025 (42%).

Our take: We foresee inflation ending the year at 3.5%, in line with the central bank’s target range. March's CPI will be published on April 6. Low inflation and anchored inflation expectations may allow the central bank to continue the easing cycle it began in January. However, recent pressures on Brent oil prices amid the US and Iran conflict could lead to a pause in the easing cycle.