2026/05/25 | Julia Passabom & Mariana Ramirez

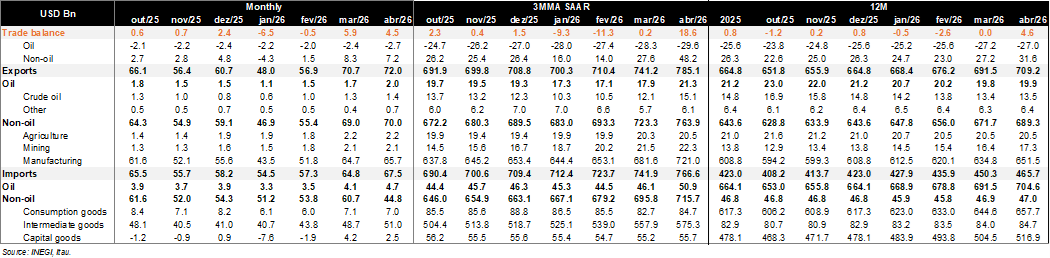

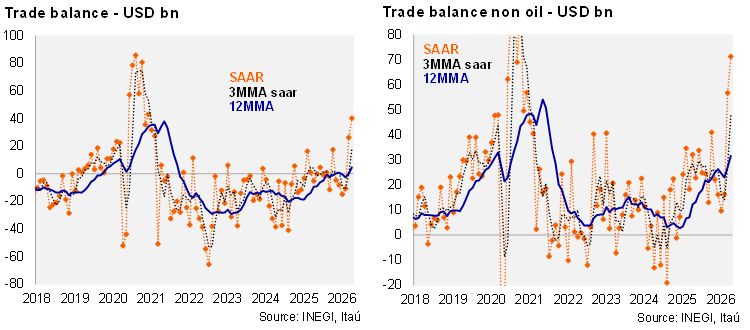

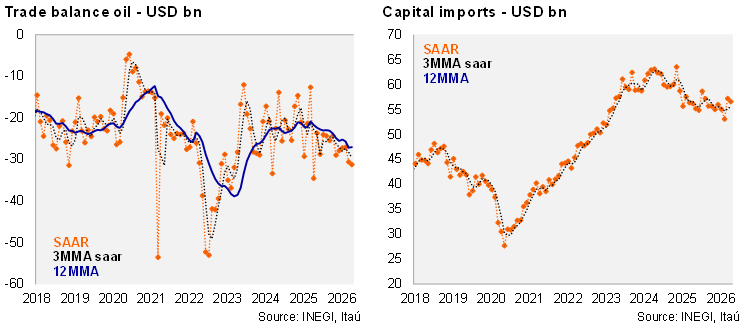

According to INEGI, Mexico recorded a USD 4.5bn trade surplus in April, significantly above market expectations (Bloomberg: USD 476mn) and a clear improvement versus the deficit observed a year ago. On a 12‑month rolling basis, the balance shifted into surplus, marking a notable recovery from near equilibrium levels seen in March. At the margin, momentum also strengthened: seasonally adjusted three‑month annualized figures show a sizeable surplus, pointing to improved external dynamics after a weak start to the year. By components, the oil balance remained in deficit, reflecting Mexico’s status as a net importer amid declining crude output, a policy focus on refining capacity, and higher international prices. In contrast, the non‑oil balance delivered a strong surplus, supported by solid performance in manufacturing and mining exports. Manufacturing shipments continued to expand, although the automotive segment remains constrained by U.S. tariffs despite ongoing efforts to increase USMCA regional content. On the import side, capital goods purchases posted a modest rebound from March but remain subdued overall, consistent with weak investment trends.

Our view: The April outturn was primarily driven by a pickup in non‑auto manufacturing exports—particularly computers and electronics—benefiting from ongoing investment in the U.S. However, elevated oil prices linked to Middle East tensions widened the oil deficit, partially offsetting non‑oil gains. Meanwhile, the second round of USMCA negotiations begins this week. U.S. Trade Representative Jamieson Greer acknowledged that discussions could extend beyond the July 1 deadline, as a full resolution appears unlikely despite efforts to narrow differences. This is in line with our baseline scenario: the agreement remains in place, but without a comprehensive conclusion by the deadline, leading to annual review cycles.

See details below