2026/06/26 | Julia Passabom & Mariana Ramirez

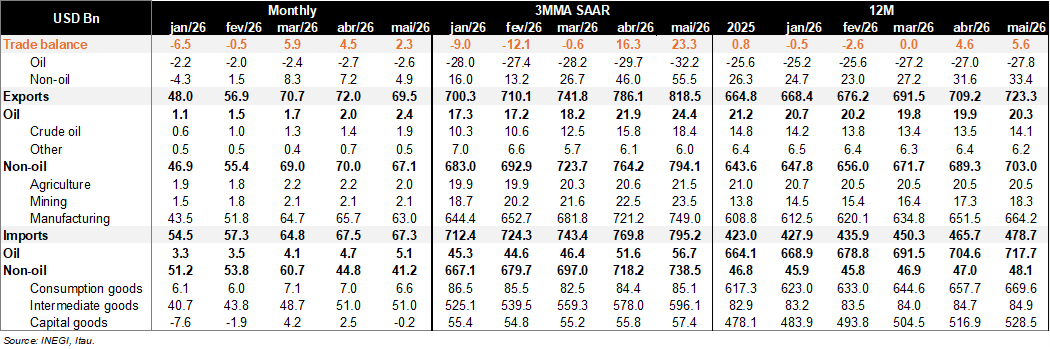

Mexico recorded a USD 2.3bn trade surplus in May, below market expectations (Bloomberg: USD 4.9bn) but above the level observed a year ago (USD 1.2bn). On a 12‑month rolling basis, the surplus remained elevated at USD 5.6bn. At the margin, momentum improved, with seasonally adjusted three‑month annualized figures pointing to a sizeable surplus, suggesting stronger external dynamics after a weak start to the year.

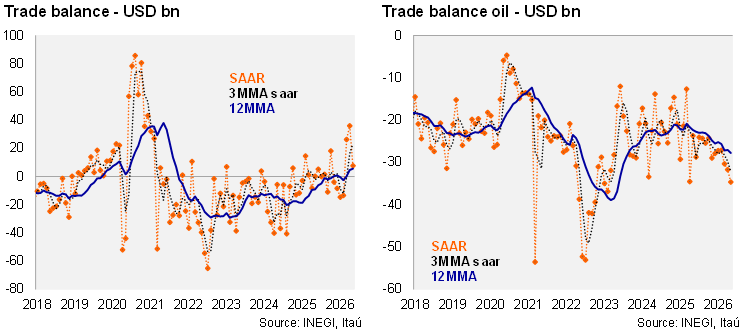

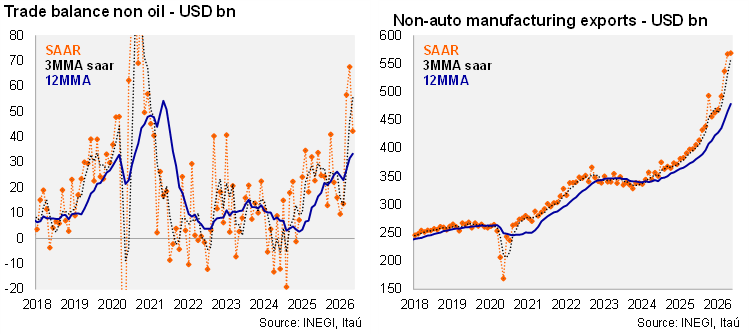

By components, the oil balance remained in deficit, reflecting Mexico’s position as a net importer amid declining crude output, a policy focus on refining, and higher international prices. In contrast, the non‑oil balance posted a solid surplus, supported by broad-based strength. Manufacturing exports continued to expand, although the automotive segment remains constrained by U.S. tariffs despite ongoing efforts to increase USMCA regional content. On the import side, capital goods rebounded from April but remain subdued overall, consistent with weak investment trends.

Our view: The May outturn was driven mainly by a rebound in non-auto manufacturing exports, particularly computers and electronics, benefiting from ongoing AI-related investment in the U.S., despite tariffs affecting the auto sector. This dynamic led us to revise our 2026 trade balance forecast to a USD 3bn deficit (from USD 5bn previously).

On USMCA, July 1 marks the formal start of the review process, when Mexico, the U.S., and Canada will exchange notifications to determine whether to extend the agreement for another 16-year period or maintain it with shorter-term reviews. In our view, annual reviews are the most probable outcome, with the U.S. leveraging the process to advance broader priorities, while Mexico seeks to anchor negotiations beyond the current U.S. administration. The next negotiation round is scheduled for July 20.

See details below