2026/05/07 | Julia Passabom & Mariana Ramirez

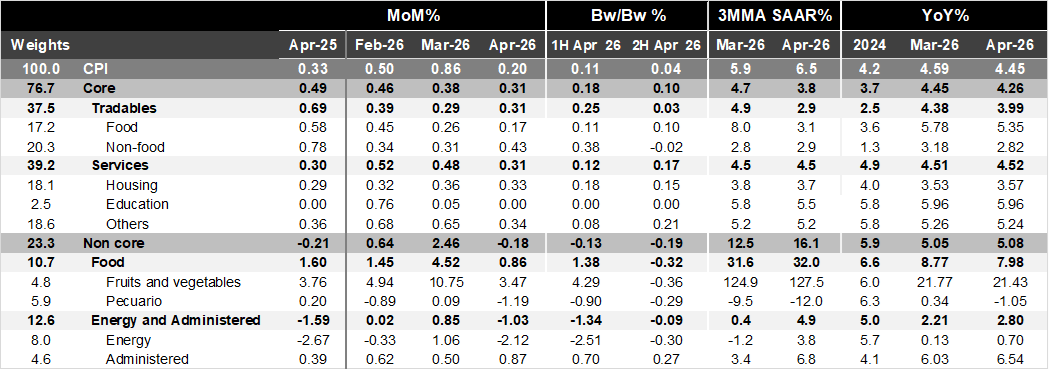

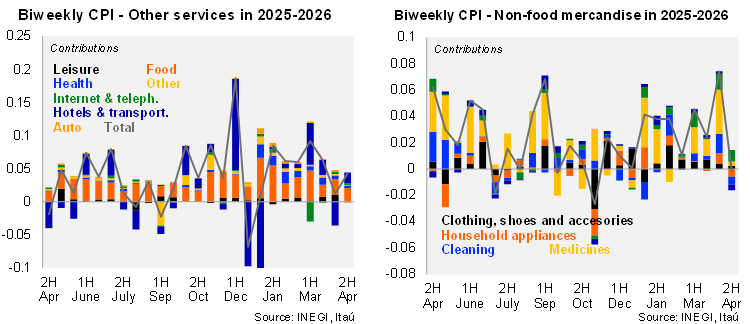

Bi-weekly headline CPI for the second half of April rose 0.04%, coming in well below the Bloomberg median (0.21%) and our estimate (0.10%). Core inflation increased 0.10%, slightly below consensus (0.12%) and broadly in line with our forecast (0.09%). Within the core basket, tradables rose 0.03% bi-weekly. Food prices posted a modest increase of 0.10%, while non-food tradables declined 0.02%, mainly driven by furniture, household appliances, and cleaning products, suggesting continued pass-through from a relatively strong peso. Core services advanced 0.17%, with housing up 0.15% and other services rising 0.21%, partly reflecting seasonal pressures ahead of the early-May holiday, particularly in hotels and transportation. Non-core CPI decreased 0.19%, driven by both energy and agricultural components. On the energy side, declines in LP gas and natural gas, alongside lower regular gasoline prices explained the deflation.

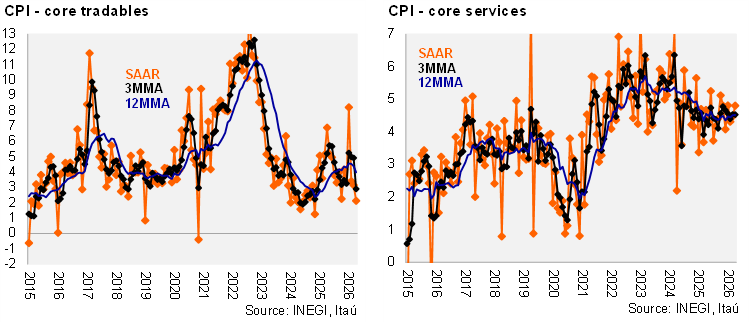

In year-over-year terms, headline inflation stood at 4.45% in April, remaining above the upper bound of Banxico’s target range, although the pace of acceleration moderated. Core inflation eased to 4.26%, led by tradables, which declined to 3.99% (from 4.38% in March), while services edged up to 4.52% (from 4.51%). On a 3-month moving average SAAR basis, core inflation improved notably to 3.8%, with tradables at 2.9% and services at 4.5%. Within services, other services were broadly unchanged, while housing and education showed some moderation, pointing to a gradual but uneven disinflation process across components.

Our take: April data reinforce the view that disinflation is progressing, albeit gradually. The easing in tradables inflation is consistent with FX strength, while other services remain stickier. Importantly, the data confirm that underlying inflation dynamics are improving at the margin without a broad-based acceleration in services, which should provide comfort to the central bank. April inflation is a key input for Banxico’s May decision. Combined with improving core dynamics, supportive FX conditions, and weak domestic demand, the data keep the door open for a 25bp rate cut, likely in a 4–1 vote split, bringing the policy stance closer to neutral, with the ex-ante real rate around the midpoint of the estimated neutral range. Banxico’s communication remains consistent with our baseline of a terminal rate of 6.5% in 2026, with rates likely to remain at that level through 2027. However, a more benign external and domestic backdrop—particularly Fed easing, FX stability, and continued favorable inflation prints—could create room for additional cuts later this year, likely as part of a new easing cycle rather than an extension of the current one, which we expect to conclude today. The Quarterly Inflation Report will be released on May 27.

See more details below