2026/05/21 | Julia Passabom & Mariana Ramirez

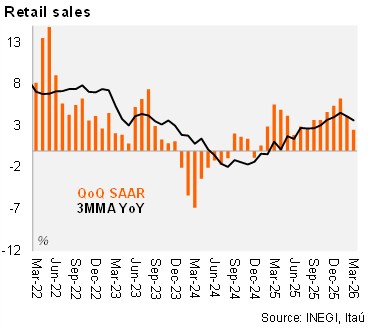

Real retail sales rose 2.9% YoY in March, broadly in line with consensus. On a seasonally adjusted basis, sales increased 0.1% MoM, undershooting the 0.4% expected. Sequentially, 6 out of 9 subsectors expanded, led by healthcare (+1.3%), household goods (+3.1%), and online sales (+4.6%). In contrast, supermarkets (-0.4%) and leisure (-6.4%) lagged, while food and beverages posted marginal growth (+0.3%). Underlying consumption fundamentals remain supportive. The real wage bill grew 6.7% YoY as of March, while real consumer credit expanded 7.1% YoY.

Our take: The data—based on a revenue survey—helps explain the divergence with IGAE (a value-added measure). While March reflects a partial rebound after February’s sharp, supply-driven contraction, underlying trends appear more resilient than headline figures suggest with q/q saar growth stands at around 2.5%, with a +2.0% carry-over for 2026. Near-term momentum remains soft, but we continue to expect a gradual recovery into 2H26, supported by domestic demand and a modest tailwind from the 2026 FIFA World Cup.

See details below