2026/05/04 | Julia Passabom & Mariana Ramirez

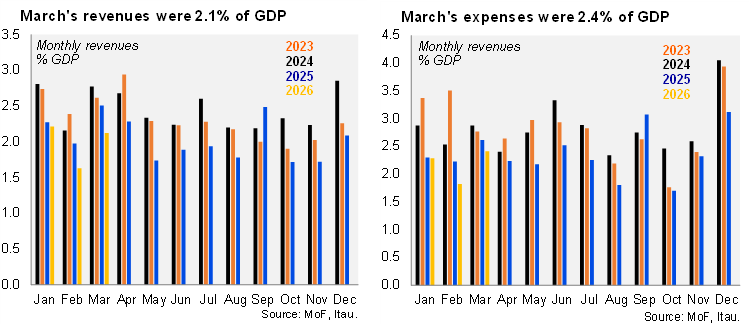

The Ministry of Finance released its March public finance report. Real revenues fell 5.1% YoY, largely reflecting low oil production and weaker corporate income tax collection. Excise taxes on sugar‑sweetened beverages, non‑caloric sweetened drinks, and tobacco products supported excise revenues on goods and services, which grew 36.5% YoY, partially offsetting the overall decline. This strength reflects both rate effects and a relatively inelastic tax base, limiting its scalability as a durable revenue source.

Gasoline and diesel revenues increased by 62% YoY, supported by higher domestic fuel prices and volumes earlier in the year, as well as elevated international oil prices. This occurred despite the federal government reactivating gasoline subsidies in mid‑March in response to the Iran–U.S. conflict, with a phased rollout by fuel type. The late‑quarter timing and the gradual implementation of the subsidies limited their offsetting effect on total fuel‑related revenues. However, this dynamic is likely to reverse if subsidies are extended or expanded, introducing downside risks to non‑oil tax revenues in coming months.

In contrast, total real spending rose 3.3% YoY, driven mainly by higher outlays in administrative branches and social programs. Capital expenditure also increased, in line with the execution schedule, supported by housing and energy‑related investment. However, March’s positive performance did not offset the notable contraction observed in January and February. Other operating expenses declined by 6.0%, which is part of the adjustment framework for fiscal consolidation. That said, expenditure compression remains uneven, with limited adjustment in structurally rigid components, raising questions about the sustainability of the consolidation effort without deeper reforms.

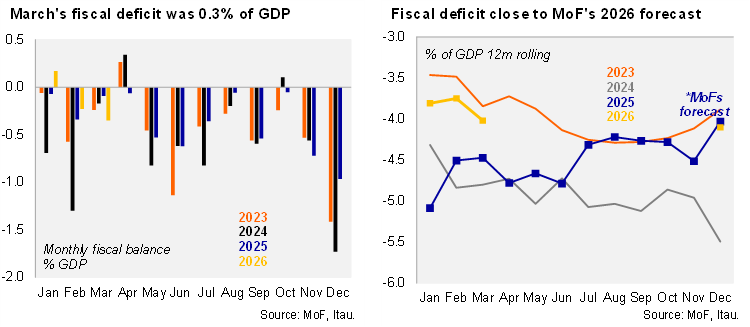

Net public sector debt stood at 50.4% of GDP, below the Ministry of Finance’s 2026 projection of 54.7%. On a rolling 12‑month basis, the broadest public balance measure (PSBR) recorded a deficit of 4.0% of GDP. While headline debt dynamics remain contained for now, fiscal buffers continue to erode amid weaker revenue trends and rising contingent liabilities.

In 1Q26, real revenues declined 0.7% YoY, running 3.5% below the level approved for the full year. Real expenditures decreased 2.6% YoY, reaching 24% of the annual approved budget, pointing to some spending restraint early in the year. Execution below target reflects both administrative delays and an implicit front‑loaded consolidation effort that may be difficult to sustain later in the year.

Our take: Monthly balances deteriorated in March relative to 2025 due to lower revenues, pointing to a challenging start to the year for revenue generation and fiscal consolidation. While near‑term oil‑related tailwinds could offer partial relief, these gains are asymmetric, as higher oil prices tend to trigger fuel subsidies that dilute the net fiscal benefit. On the expenditure side, the sharp retrenchment in public investment occurred ahead of the execution of the Infrastructure Investment Plan for 2026–2030. This plan is not included in the current budget and is projected to allocate an additional 2% of GDP. Given past experience, where similar initiatives were only partially executed, credibility risks remain elevated. Given natural lags in capex implementation, reaching the full 2% of GDP in 2026 appears ambitious. Looking ahead, attention will turn to the 2027 budget, scheduled for release before September 8. The 2027 pre‑budget reinforces a continuity narrative rather than a policy shift, maintaining a gradual fiscal consolidation path after the 2024–2025 expansion. The final fiscal parameters for 2027 will be defined in the budget proposal to be submitted in September. While the consolidation framework remains formally intact, its credibility will increasingly hinge on execution capacity, political discipline, and the government’s willingness to absorb near‑term growth trade‑offs in a more complex macro‑financial environment.

See detailed data below