2026/05/22 | Julia Passabom & Mariana Ramirez

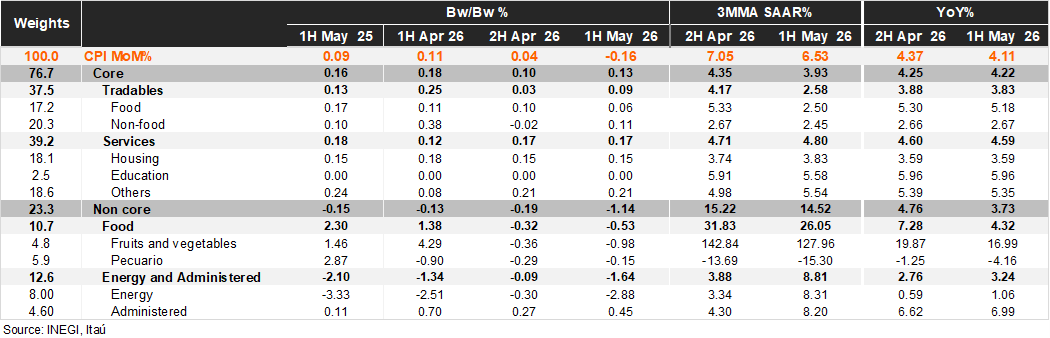

Bi-weekly headline CPI for the first half of May declined 0.16%, slightly above the Bloomberg median (-0.18%) and below our estimate (-0.12%). Core inflation increased 0.13%, slightly below consensus (0.15%) and in line with our forecast. Within the core basket, tradables rose 0.09% bi-weekly, with food prices posting a modest increase of 0.06% and non-food tradables rising 0.11%, partly reflecting a rebound in cleaning products after the previous print’s deflation. Core services advanced 0.17%, with housing up 0.15% and other services increasing 0.21%, likely influenced by seasonal pressures related to early-May holidays, particularly in transportation. Non-core CPI fell sharply by -1.14%, driven by both energy and agricultural components. Electricity prices declined on the back of seasonal subsidies amid the hot season, while agricultural prices fell on the back of deflation in key items such as green tomatoes, chili peppers, lemons, and onions.

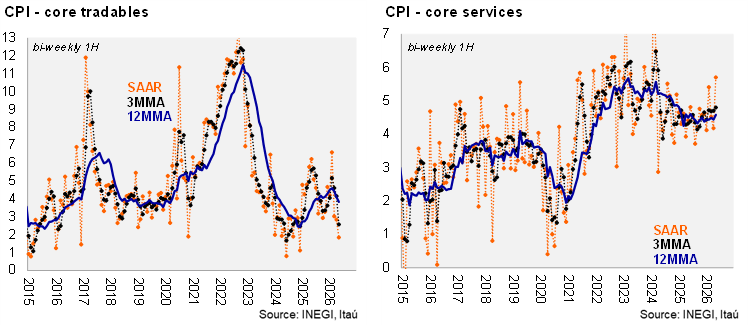

In year-over-year terms, headline inflation printed at 4.11%, remaining above the upper bound of Banxico’s target range, although the pace of acceleration moderated. Core inflation eased to 4.22%, driven by tradables, which declined to 3.83% (from 3.88% previously), while services remained broadly stable at 4.59% (from 4.60%). On a 3-month moving average SAAR basis, core inflation improved to 3.93%, with tradables at 2.58% and services at 4.80%, highlighting continued divergence across components. Within services, pressures in housing and other services persist, while education showed signs of moderation—consistent with a gradual but uneven disinflation process.

Our take: The print reinforces a gradual disinflation narrative, with tradables continuing to benefit from FX strength and easing goods inflation, while services inflation remains sticky. We maintain our year-end inflation forecast at 4.1%. Looking ahead, the Quarterly Inflation Report on May 27 will be key; we expect a downward revision to 2026 GDP closer to 1% (from levels nearer 2%), potentially widening the output gap and reopening the discussion around a renewed easing cycle.

See more details below