2026/03/26 | Julia Passabom, Mariana Ramirez &

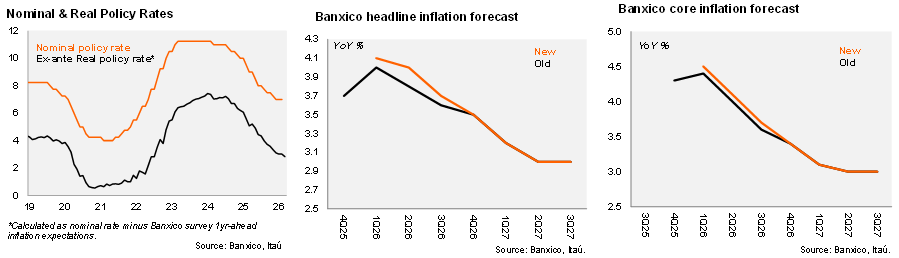

In its March meeting, Banxico’s Board cut the policy rate by 25 bps to 6.75%, contrary to both market consensus (48% expected a rate cut) and our expectation that it would remain unchanged. The decision was divided, with board members Borja and Heath voting to keep the rate unchanged (in the previous rate cut, only Heath was the opposing board member). Despite the ongoing conflict in the Middle East, the board considered that “the monetary policy stance attained is adequate to face the challenges posed by an extension and escalation of the Middle Eastern conflict and its outcome.” The forward guidance signaled that the easing was “on this occasion,” while changing the plural form of “adjustments” to the singular “an additional reference rate cut” regarding future policy actions. This wording suggests that the Board envisions only one additional rate cut ahead.

Banxico introduced upward revisions to its 1Q26 and 2Q26 inflation forecasts due to pressures from non-core inflation and persistent services inflation, while maintaining the convergence of headline inflation to the 3% target for the second quarter of 2027. The balance of risks to the inflation forecasts is now considered "biased up" from "more balanced, but still biased up" in the previous statement. Among the upside risks to inflation, they included the inflationary impact of geopolitical conflicts.

Our take: The tone of the statement—highlighting that the rate cut is appropriate "on this occasion" and introducing the singular "an additional reference rate cut"—suggests that the rate-cutting cycle is nearing its end. In our view, Banxico's decision reflects a prioritization of domestic economic conditions over inflationary risks stemming from the geopolitical conflict. We continue to expect an additional rate cut this year. The meeting minutes will be published on April 9, and the quarterly inflation report on May 27. The next monetary policy meeting will be held on May 7.