2026/03/13 | Julia Passabom, Mariana Ramirez &

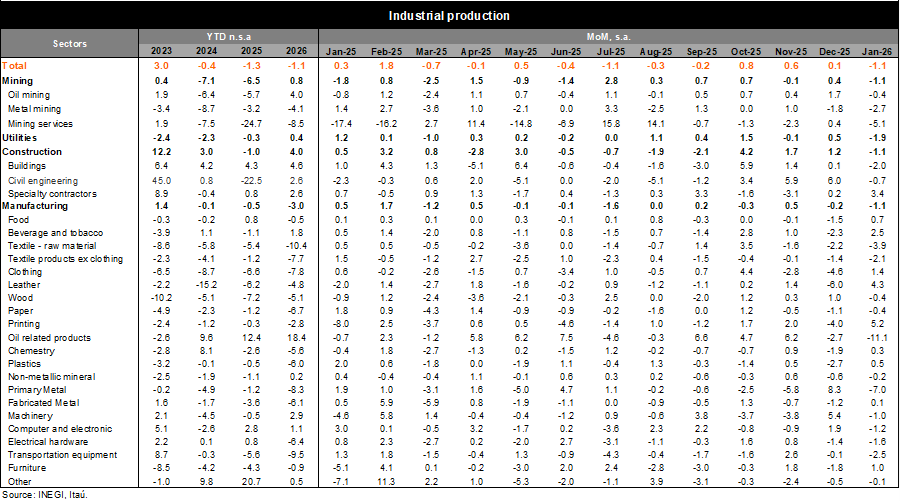

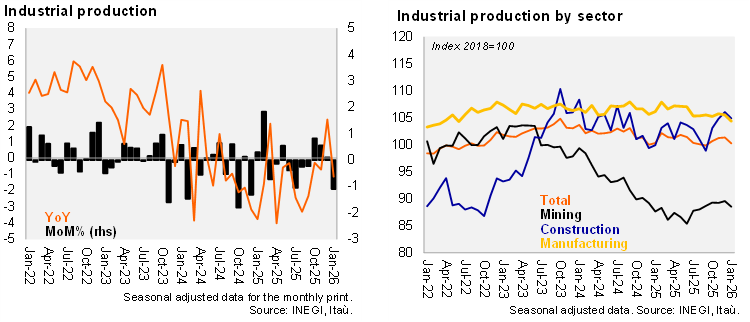

Industrial production (IP) decreased by 1.1% YoY in January, falling short of Bloomberg’s market consensus of a 1.6% expansion. This decline was primarily due to a 3.0% contraction in manufacturing, with 14 out of 21 subsectors experiencing declines. Meanwhile, other sectors rose at the margin: mining increased by 0.8%, utilities by 0.4%, and construction by 4.0%. Using seasonally adjusted figures, IP decreased by 1.1% MoM, underperforming compared to the consensus expectation of 0.1% growth and INEGI’s nowcast of +0.4%. This performance was driven by a broad-based contraction: mining fell by 1.1% MoM, construction by 1.1% (with declines in buildings and civil engineering), manufacturing by 1.1% (as 12 out of 21 subsectors decreased), and utilities by 1.9%.

Our take: Despite today’s negative surprise, industrial production remains in positive territory, with the QoQ/SAAR at +2.9% compared to 4.0% in December. Among sectors, only manufacturing contracted sequentially (-0.6%, QoQ/SAAR). Looking ahead, construction is expected to expand, supported by public infrastructure spending in sectors such as energy, railways, highways, ports, health, water, education, and airports. Manufacturing, on the other hand, should recover with the reduction in trade uncertainty in the second half of the year. We maintain our view of a gradual GDP upswing this year to 1.5%, supported by continued strong growth in the US and a marginal boost from the 2026 World Cup. However, an escalation of geopolitical events could have negative effects on the economy.

See more details below: