2026/03/24 | Julia Passabom, Mariana Ramirez &

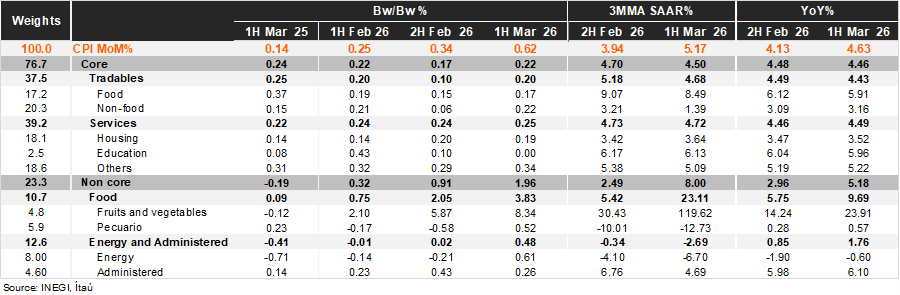

Bi-weekly headline CPI for the first half of March was 0.62%, well above the Bloomberg median of 0.40% and our estimate of 0.42%. In contrast, core CPI rose by 0.22%, in line with market expectations and below our estimate of 0.27%. Within the core component, tradables rose 0.20% bi-weekly, with the food subcomponent rising 0.17% and non-food increasing 0.22%. Meanwhile, core services advanced 0.25% bi-weekly, with housing and other categories increasing by 0.19% and 0.34%, respectively. Non-core CPI recorded a 1.96% rise, the highest inflation since the first half of July 2024, driven by food prices in products such as tomatoes, potatoes, green tomatoes, and lemons, while energy and tariff inflation rose by 0.48%, mainly due to pressures from electricity.

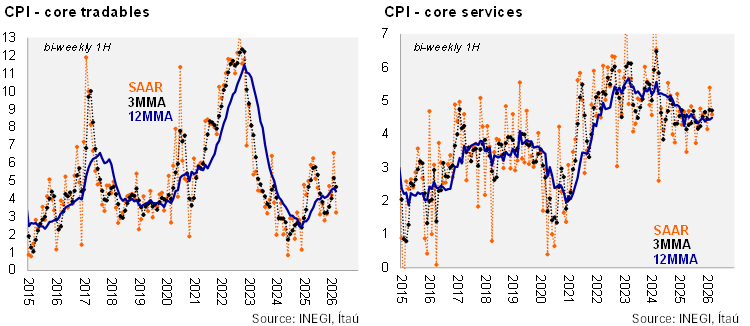

In annual terms, headline inflation was 4.63% in the first half of March, exceeding the upper bound of the inflation target’s tolerance range and marking the highest level since the second half of October 2024. Core CPI was 4.46%, with tradables at 4.43% (slightly down from 4.49%) and services at 4.49% (slightly up from 4.46%). Core measures showed marginal relief: core CPI was at 4.50% on a 3MMA SAAR basis, with tradables at 4.68% and services at 4.72%. Within services, other service categories showed a slightly better performance (5.09% vs. 5.38% in the first half of March).

Our take: Today's report revealed an upside surprise in the non-core component due to supply shocks affecting fruits and vegetables, specifically a reduced supply in one of the main tomato-producing states, along with road blockades related to protests over insecurity. The main surprise came from a single product: tomatoes, which contributed to 0.22 pp to headline. While recent inflation data show no significant second-round effects from excise taxes and tariffs on imports from non-FTA countries, geopolitical risks have increased. In this context, Banxico is likely to pause at the next meeting and shift its inflation risk balance to the upside to reflect external uncertainties. We continue to expect a terminal rate of 6.5% in 2026, with rates likely to remain at that level through 2027.

See more details below