2026/05/12 | Julia Passabom & Mariana Ramirez

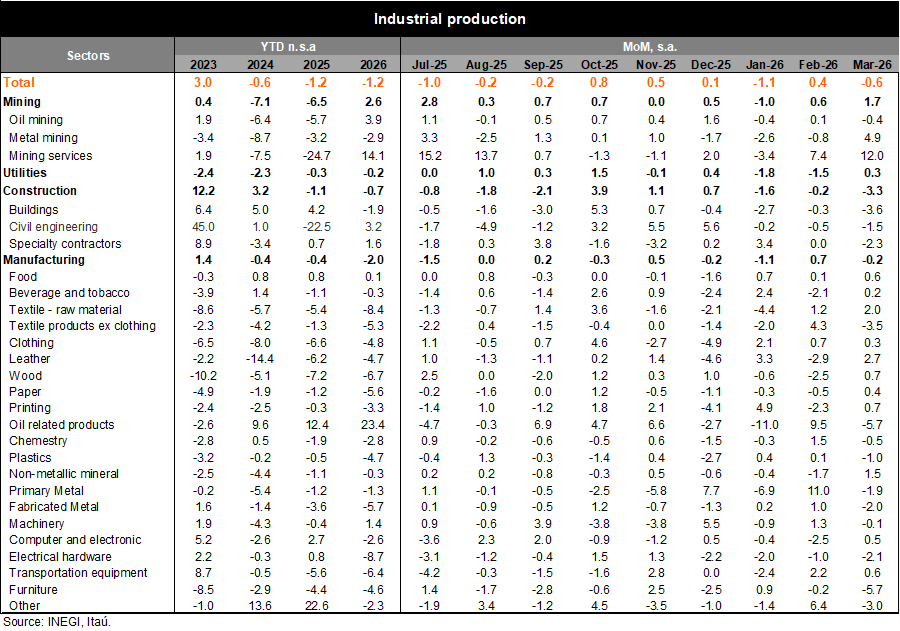

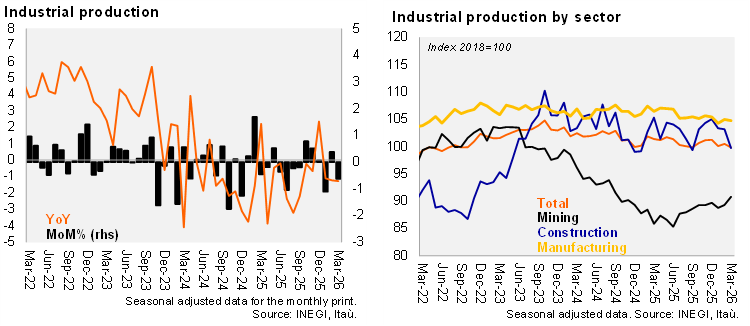

Industrial production (IP) declined by 1.3% YoY in March, in line with Bloomberg’s median but slightly below our call (-0.9%). The weakness was driven by manufacturing (-1.0% YoY), with 16 of 21 subsectors contracting, and construction (-6.2% YoY), dragged down by edification and specialty contractors. Mining (+6.0% YoY) and utilities (+0.2% YoY) provided only modest offsets. Historical revisions show weaker performance in 2024 (‑0.6% vs. +0.4% previously) and a marginal upward adjustment for 2025 (-1.2% vs. -1.3%).

On a seasonally adjusted basis, IP fell 0.6% MoM, in line with our expectations and below INEGI’s nowcast (+0.1%). The decline was led by construction (-3.3% MoM) and manufacturing (-0.2%, with 10 of 21 subsectors contracting). Mining rose 1.7% MoM despite weakness in oil, while utilities rebounded 0.3% after two consecutive declines.

Our take: The data confirm a weak start to the year for the industrial sector, which continues to weigh on overall activity. On a quarterly basis, sharp contractions persist in manufacturing (-5.3% QoQ SAAR), utilities (-9.8%), and construction (-8.0%). Despite this soft backdrop, recent data revisions—including the goods and services account—suggest a slightly less negative contribution of industry to 1Q26 GDP than initially estimated (-0.8% QoQ SA flash). We expect a modest upward revision to around -0.7% QoQ SA in 1Q26 GDP, to be released on May 22. Looking ahead, we expect momentum to improve in the second half of the year, with construction supported by public infrastructure spending and manufacturing gradually recovering as trade uncertainty fades. We maintain our 1.1% GDP growth forecast for 2026.

See more details below