2026/02/11 | Julia Passabom, Mariana Ramirez & Ignacio Martínez

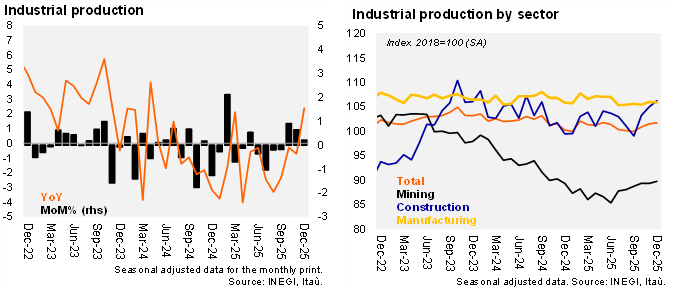

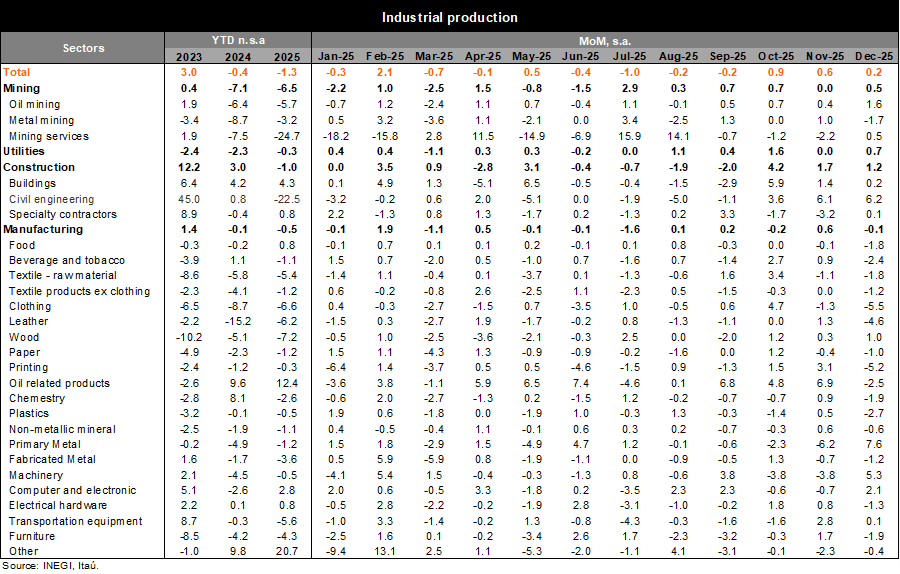

Industrial production (IP) rose by 2.4% YoY in December, above Bloomberg’s median (1.9%). Using seasonally adjusted data, IP increased by 0.2% MoM in the month, well above the consensus of a 0.2% sequential contraction. This positive sequential performance was driven by mining (+0.5%) and construction (+1.2%), while manufacturing fell by 0.1%. In 4Q25, overall industrial production rose by 4.9% QoQ/SAAR (-5.2% in 3Q25) with mining increasing by 5.8% (8.1% in 3Q25), manufacturing rising 1.2% (-6% in 3Q25) and construction increasing 17.3% (-2.6% in 3Q25).

IP contracted in 2025, for the second consecutive year. Industrial production fell by 1.3% in 2025, following the 0.4% contraction in 2024. By sector, last year’s data showed broad-based declines, with mining contracting by 6.5% (-7.1% in 2024), construction falling by 1% (+3% in 2024) and manufacturing with -0.5% (-0.1% in 2024).

Our take: Our forecast considers a gradual improvement in economic activity this year in Mexico, which seems to be supported by an acceleration at the margin in IP. However, two consecutive years of annual IP contractions take place in the context of a negative fiscal impulse and significant USMCA policy uncertainty, which we expect to linger in the near term. The better relative performance of manufacturing is likely related to its linkages with economic activity in the US, which, in turn, has broadly outperformed. The recently announced infrastructure investment plan may boost investment, especially in energy, although greater clarity on the timing, financing, and investment vehicles would help. We project GDP growth of 1.5% in 2026.