2026/03/31 | Julia Passabom, Mariana Ramirez &

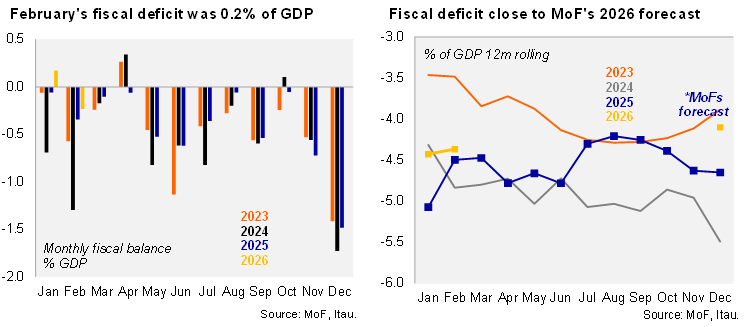

The Ministry of Finance (MoF) released its public finance report for February. On a 12-month rolling basis, the broadest measure of the public balance (PSBR) posted a deficit of 4.4% of GDP in February, while the primary balance stood at 0.5% of GDP.

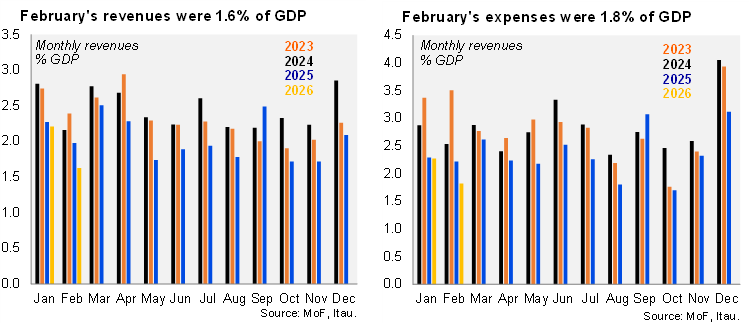

On the revenue side, real collections declined by 7.2% YoY in February. This contraction was largely driven by the sharpest drop in oil-related revenues since 2020 and the weakest performance of VAT revenues since 2009. The latter reflects the peso’s appreciation as well as base effects stemming from last year's stronger VAT performance. Expenditure dynamics also reflected a contractionary stance. Total real expenditure decreased by 7.5% YoY, mainly due to a steep decline in capital investment, which marked its worst performance since 1990. Finally, net government debt stood at 49.8% of GDP, remaining below the MoF’s 2026 forecast of 52.3%.

Our view: February’s data point to a difficult start to the year for revenue generation and fiscal consolidation efforts. However, near-term oil-related tailwinds could offer partial relief. The 2026 Budget assumes a crude price of USD 54.9 per barrel; each additional dollar per barrel translates into roughly 11.6 billion pesos (≈0.04% of GDP) in extra government revenue. Under a scenario where average crude prices permanently reach USD 90/bbl, ceteris paribus, additional revenues could approach 400 billion pesos (≈1.4% of GDP). However, this gross benefit will be substantially eroded if the government expands fuel tax incentives or subsidies to shield domestic prices. The current fiscal position leaves limited room to finance large-scale subsidies without material trade-offs elsewhere in the budget.

On the expenditure front, the sharp retrenchment in public investment occurred ahead of the execution of the Infrastructure Investment Plan for 2026–2030. This plan is not included in the current budget and is projected to allocate an additional 2% of GDP this year. In the past, similar announcements were only partially executed. We are awaiting additional details on the plan to assess its impact on our forecasts – given natural lags in capex implementation, reaching the full 2% in 2026 seems ambitious.

Looking ahead, attention will turn to the 2027 pre-budget, schedule for release before April 8. This framework is expected to face meaningful challenges, as the scope for further fiscal tightening appears limited amid weaker revenues and rising spending pressures.

See more details below