2026/04/23 | Julia Passabom & Mariana Ramirez

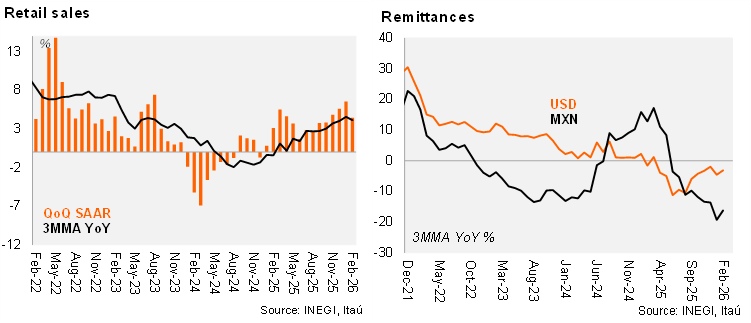

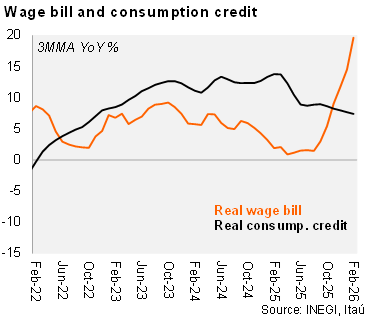

According to a survey of commercial establishments, real retail sales increased 3.1% YoY in February, undershooting Bloomberg consensus (4.5%). On a seasonally adjusted basis, sales fell 0.9% MoM, a sharper contraction than the ‑0.2% expected by the consensus. Sequentially, seven of nine subsectors posted declines, led by food and beverages (‑4.3%), health care items (‑3.7%), and textiles and apparel (‑1.7%). In contrast, supermarkets (+0.2% MoM) and household goods (+1.3%) recorded gains. However, despite the weak monthly print, consumption fundamentals remain supportive. The real wage bill surged 26.9% YoY in February due to a low base effect in employment and the minimum wage increase of 13%; while real consumer credit from commercial banks expanded 6.9% YoY, cushioning the downside to household demand.

Our take: The release is based on a company revenue survey, which helps explain the divergence with IGAE figures that track value added. Despite the negative headline surprise, the underlying signal is less concerning: quarterly growth annualized stands at 4.5%, with a statistical carry‑over of +2.0% for the year. That said, in light of soft industrial production data and weakening leading indicators, we still expect GDP to contract 0.3% QoQ in 1Q, introducing a downside bias to our 2026 GDP forecast of 1.5% YoY. Looking ahead, momentum should improve in the second half of the year. Construction activity is likely to pick up gradually, supported by higher public infrastructure spending across energy, transport, ports, health, water, education, and airports. Manufacturing should also recover as trade uncertainty eases, allowing investment conditions to stabilize.