2026/05/25 | Julia Passabom & Mariana Ramirez

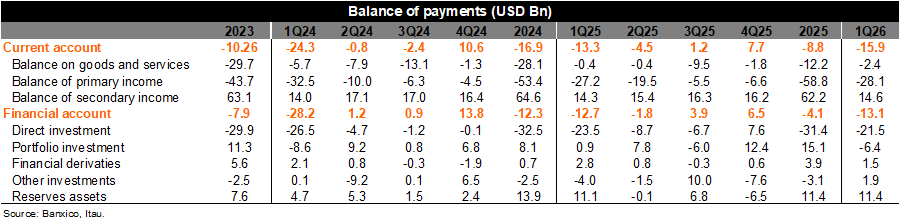

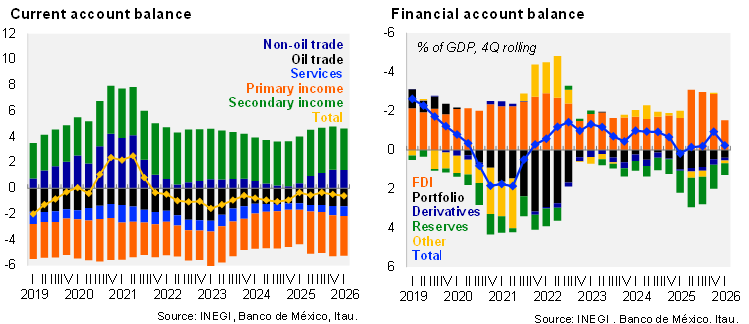

The current account posted a deficit of USD 15.9 billion in 1Q26, slightly wider than Bloomberg’s consensus of USD 15.5 billion. Compared with 1Q25, the wider deficit was mainly driven by a deterioration in the oil trade, services, and primary income balances, all of which recorded shortfalls. This was largely offset by stronger surpluses in the non‑oil trade balance and secondary income, supported by continued momentum in manufacturing exports and resilient remittance inflows, helping cushion the overall external position. As a result, the current account deficit stood at 3.1% of GDP in the 1Q26, broadly unchanged from a year earlier. Within the current account, annual comparisons confirm that the weakening in oil‑related trade, services, and primary income was partially compensated by improved balances in non‑oil goods and secondary income.

On the other hand, the financial account registered a net borrowing requirement of USD 4.1 billion in 1Q26, reflecting mixed capital flow dynamics. By components, foreign direct investment remained the main source of financing, with net inflows of USD 21.5 billion, although composition suggests some moderation in new investment and intercompany flows. In contrast, portfolio investment recorded net outflows of USD 6.4 billion, pointing to continued volatility in global financial conditions and investor repositioning amid uncertainty around trade policy and interest rates. At the same time, reserve assets increased by USD 11.4 billion, indicating FX accumulation—likely supported by valuation effects and central bank operations—while financial derivatives posted a net inflow of USD 1.5 billion, helping offset part of portfolio outflows. Other investment flows also contributed to the adjustment, reflecting cross‑border liquidity movements and corporate financing decisions. The errors and omissions balance of USD 1.1 billion helped close the gap.

Our view: Today’s release highlights some constructive elements. In particular, front‑loaded demand and AI‑related investment in the U.S. continue to support non‑auto manufacturing exports—especially in electronics—explaining the strength in the non‑oil trade balance. At the same time, remittances remain robust, underpinned by a still‑resilient U.S. labor market. However, as expected, FDI moderated slightly in 1Q26 relative to 2025, mainly reflecting weaker greenfield investment and softer intercompany flows amid heightened global and domestic uncertainty. Looking ahead, we expect capital flows to remain volatile, particularly in portfolio investment, while FDI is likely to stay cautious as firms delay decisions amid unresolved USMCA negotiations and a still uncertain global backdrop. We maintain our forecast for a current account deficit of 0.6% of GDP in 2026, consistent with a trade deficit of around USD 5 billion.

See details below