2026/06/24 | Julia Passabom & Mariana Ramirez

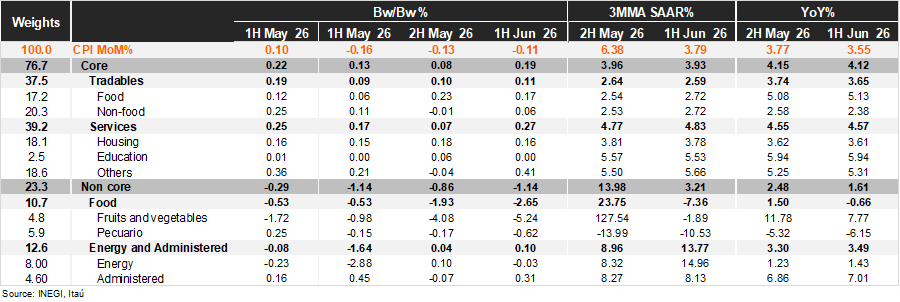

Bi-weekly CPI for 1H June printed at -0.11%, undershooting both consensus (+0.05%) and our forecast (+0.10%). Core rose 0.19%, slightly below expectations (consensus: 0.20%; Itaú: 0.20%). Within core, tradables increased 0.11%, with food up 0.17% and non-food up 0.06% following prior discount-driven deflation. Core services rose 0.27%, led by pressures in air transportation, hotels, and tourism-related services amid stronger demand likely linked to the World Cup. Non-core fell 1.14%, driven by declines in agricultural goods (e.g., tomatoes and chili) and livestock (e.g., eggs).

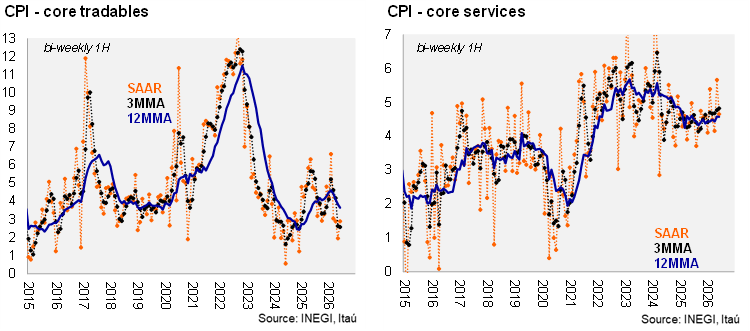

On an annual basis, headline inflation came in at 3.55%, below Banxico’s upper target band, while core eased to 4.12%. Tradables declined to 3.65%, while services edged up to 4.57%, highlighting a persistent divergence between the categories. On a 3-month SAAR basis, core held at 3.79%, with tradables at 2.59% and services at 4.83%, underscoring ongoing stickiness in services despite some moderation in education.

Our take: The print reinforces a gradual disinflation trend, mainly driven by goods, which continue to benefit from FX strength. Services remain sticky, pointing to an uneven path ahead. We maintain our 4.1% year-end inflation forecast, although weather-related risks (e.g., El Niño) could add pressure later in the year.

See more details below