2026/05/06 | Julia Passabom & Mariana Ramirez

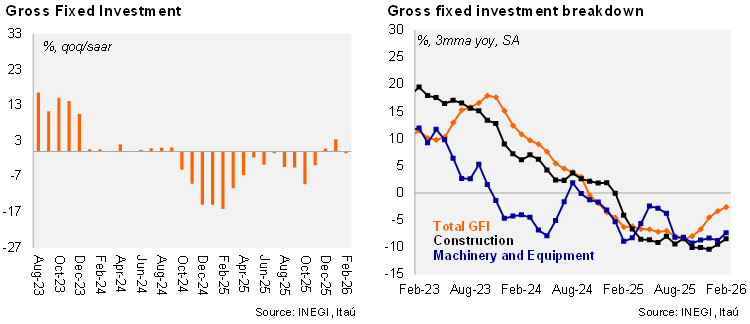

Gross Fixed Investment (GFI) decreased by 4.2% YoY in February, a steeper decline than the Bloomberg median (-2.7%). By sector, machinery, and equipment fell by 9.7%, with both imported and domestic components contracting. Construction grew by 1.1% YoY, led by increases in public and residential segments. On a seasonally adjusted basis, investment declined by 0.8% MoM, below market expectations of -0.4%. Machinery and equipment fell by 2.3% m/m, reflecting a combination of weaker external demand, tariff-related distortions, and a stronger peso that likely dampened import substitution dynamics, while construction edged up by 0.1% m/m, supported by residential activity.

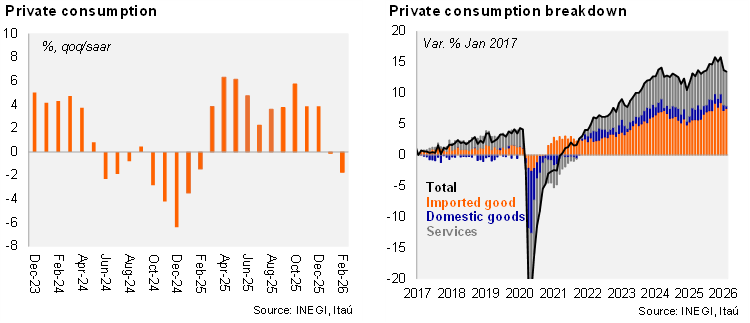

Private consumption increased by 0.9% YoY, below the Bloomberg median of +2.0%. On a monthly basis (SA), private consumption declined by 0.5%, marking a second consecutive contraction after January and undershooting INEGI’s nowcast (+0.2%). At a granular level, domestic goods and services contracted by 0.9% and 0.3%, respectively, while imported goods rose by 1.9%, partially reversing January’s decline following the front-loading and subsequent normalization after the tax increase on imports from non-FTA countries.

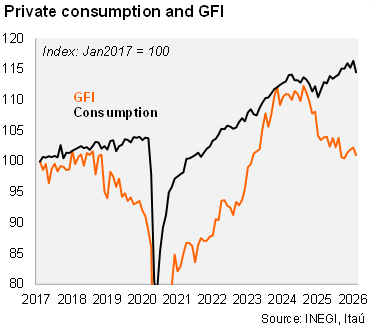

Our view: February’s domestic demand data point to a broad-based loss of momentum, driven by a mix of policy and transitory shocks. These include changes in tariffs on imports from non-FTA countries, peso appreciation, tighter global financial conditions at the margin, US trade measures weighing on the heavy-vehicle segment, and localized security disruptions in the Pacific and Bajío regions following the capture of a major cartel leader in February.

Looking ahead, high-frequency indicators suggest a tentative stabilization rather than a clear rebound. Administrative records show domestic light vehicle sales grew 1.4% (12-month moving average) in March, indicating that durable consumption remains resilient but lacks strong acceleration. In addition, capital goods imports improved slightly in March, which, if sustained, could signal a floor in the investment cycle.

On policy, the recently announced Infrastructure Investment Plan for 2026–2030 introduces an upside risk to activity in 2H26 through improved execution and project pipeline visibility, although the impact is likely to be gradual. Private consumption is expected to continue expanding at a moderate pace, supported by real wage gains and temporary demand tailwinds linked to the World Cup in mid-year. Overall, we maintain a cautious macro-outlook, with growth constrained by weak domestic demand dynamics, limited fiscal space, and lingering external uncertainty, and forecast 2026 GDP growth at 1.1% YoY.

See details below