2026/03/05 | Julia Passabom, Mariana Ramirez & Ignacio Martínez

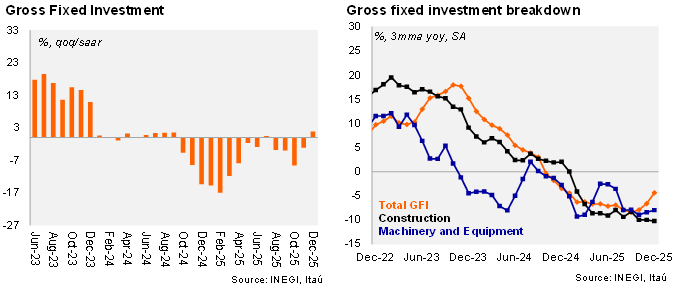

Gross Fixed Investment (GFI) slightly decreased by 0.01% YoY in December, slightly weaker than the Bloomberg median (0.0%). By sector, machinery and equipment decreased by 4.6%, with both imported and domestic components declining. Construction rose by 4.3% YoY, with private and residential components also increasing. Using seasonally adjusted data, investment increased by 0.5% MoM, somewhat below market expectations of +0.8%. Machinery and equipment decreased by 0.3%, while construction rose by 0.9% due to both residential and non-residential components.

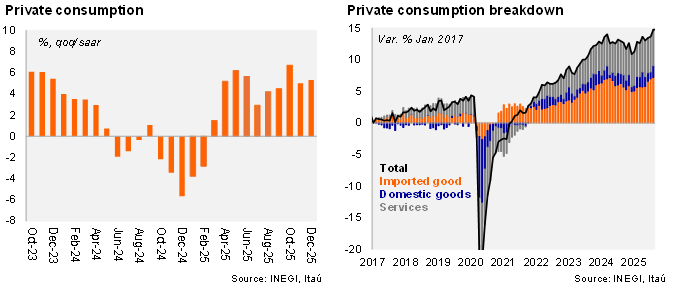

Private consumption increased by 6.8% YoY, well above Bloomberg median (4.5%). On a monthly basis, using seasonally adjusted data, private consumption rose by 1.2%, with domestic goods and services showing growth of 0.1% and 0.2%, respectively. Imported goods grew by 4.9%, possibly due to frontloading of purchases before the tax increase on imported goods from countries without trade agreements, which came into effect in January 2026.

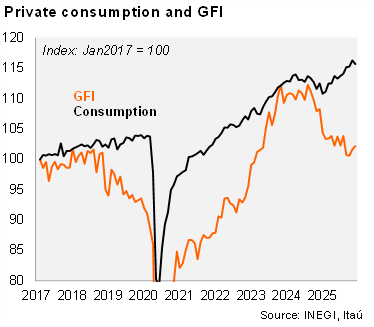

Our view: December's domestic demand figures showed positive dynamics across components, with investment at 1.8% QoQ/SAAR (up from -3.1%) and private consumption positive at 5.3%, up from 5.0% in November. Looking ahead, however, soft capital goods imports suggest private investment is likely to remain subdued. In this context, the recently announced Infrastructure Investment Plan for 2026–2030 poses an upside bias to our activity forecasts for the second half of the year. Private consumption, on the other hand, is expected to continue growing at moderate rates, supported by rising wages. We forecast 2026 GDP growth at 1.5% YoY.

See details below