2026/06/25 | Julia Passabom & Mariana Ramirez

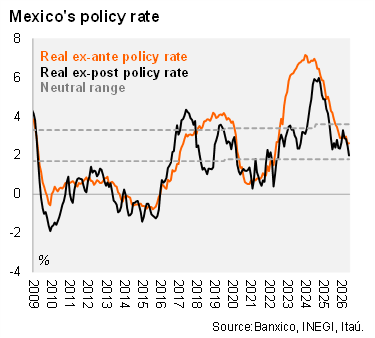

Banxico kept the policy rate at 6.50% at its June meeting, in line with consensus and our call. The decision was unanimous following two consecutive divided decisions. The forward guidance reinforces a ‘hold for longer’ stance after concluding its easing cycle in May, as the board judges that the current monetary policy stance is well-suited to face the challenges posed by the macroeconomic environment and consistent with a gradual convergence of inflation toward the target.

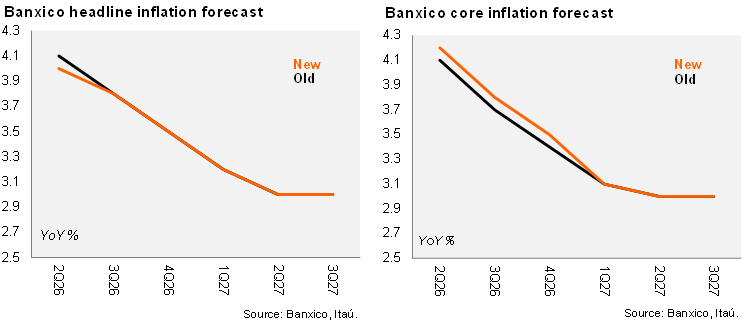

Banxico revised its short-term headline inflation forecasts slightly lower in 2Q to reflect softer-than-expected non-core pressures, while core projections were revised slightly upwards in 2Q and 4Q, suggesting persistent underlying price dynamics. However, the board maintained its timeline for convergence to the 3% target in 2Q27, implicitly reaffirming that disinflation will remain gradual. The balance of risks remains skewed to the upside. Within the risk assessment, climate-related disruptions moved up to third place (from fifth), followed by cost pressures and peso depreciation, highlighting increased concern around weather-related shocks.

Our take: The statement reflects a neutral stance with limited conviction for further near-term adjustments and a “higher-for-longer” bias unless inflation surprises materially. We continue to see the policy rate at 6.50% through 2027, consistent with Banxico’s cautious reaction function. Despite the market pricing in two Fed hikes this year, we see a potential sharp depreciation of the peso as the main trigger for renewed tightening by Banxico. Absent FX pressures, the bar for hikes remains high. In our view, the bias is still tilted toward easing, conditional on FX stability and further progress in core disinflation. The next key events are the minutes of this meeting on July 9 while the next policy meeting is scheduled for August 6.

See more details below