2026/05/07 | Julia Passabom & Mariana Ramirez

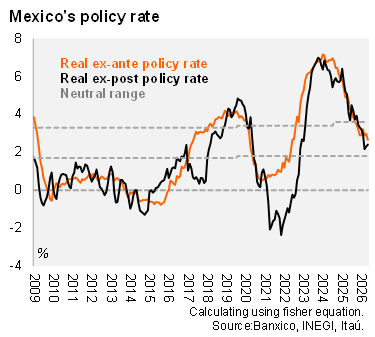

Banxico cut the policy rate by 25bps to 6.50% at its May meeting, in line with both consensus and our call. The decision was split, with board members Jonathan Heath and Galia Borja again dissenting in favor of holding rates. With this move, the monetary policy rate falls to the center of the neutral rate range, as the ex-ante real rate now sits in the midpoint of the Bank’s estimated neutral range (2.7%). The Board’s rationale centered on weak economic activity, the cumulative tightness of monetary conditions, stable FX dynamics, and an improving inflation outlook. Importantly, forward guidance pointed to this move as the end of the current easing cycle.

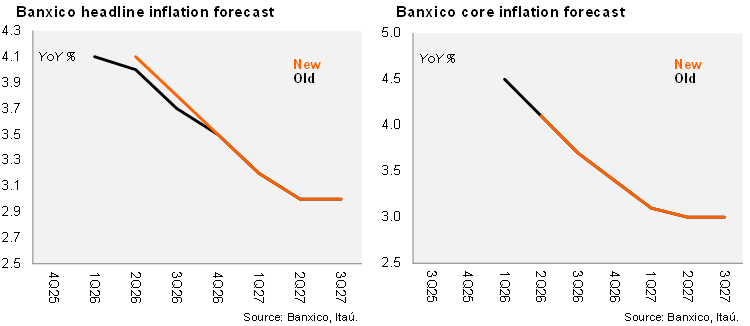

Banxico revised its short-term headline inflation forecasts slightly higher, mainly reflecting stronger-than-expected non-core pressures, but maintained its timeline for convergence to the 3% target in 2Q27. The balance of risks remains skewed to the upside. Within the risk assessment, core inflation persistence moved up to the second position (from third), followed by cost pressures, while the rest of the risk map was unchanged.

Our take: The statement clearly frames this cut as the terminal move of the cycle, and we continue to expect the policy rate to remain at 6.5% through 2027. That said, the outlook remains uncertain. A more benign external and domestic backdrop—particularly Fed easing, continued FX stability, and further progress in core disinflation—could reopen the door for additional cuts later this year, but likely under a new easing phase rather than an extension of the current one. The next key events are the Quarterly Inflation Report on May 27 and the June 25 policy meeting.

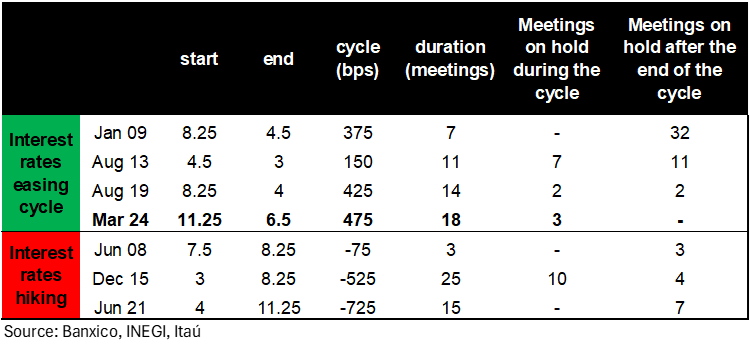

From a broader perspective, this has been one of the most prolonged easing cycles in recent history. Cumulative cuts are approaching 475 basis points, among the deepest on record, but delivered gradually across a large number of meetings. Notably, only around 17% of decisions resulted in a hold, pointing to a relatively continuous easing bias compared to past cycles. This underscores a central bank that remains data-dependent but has shown greater willingness to adjust policy in a steady, iterative manner rather than relying on frequent pauses.

See more details below