2026/04/30 | Julia Passabom & Mariana Ramirez

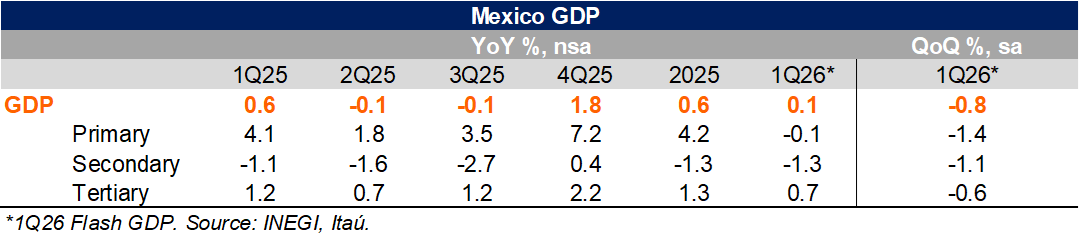

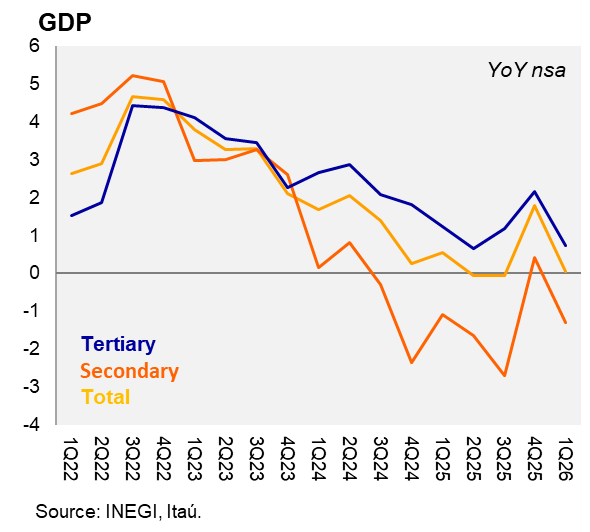

The 1Q26 flash GDP expanded by 0.1% YoY, below Bloomberg’s market consensus of 0.7%, but in line with our forecast. By sector, primary activities edged down 0.1% YoY, industrial output contracted 1.3%, and services grew 0.7%, underscoring an uneven growth profile. On a seasonally adjusted quarterly basis, GDP contracted by 0.8% QoQ (Bloomberg: ‑0.6%, Itaú: ‑0.7%), reflecting a broad‑based slowdown. Industry declined 1.1%, services fell 0.6%, and agriculture dropped 1.4%, pointing to weak underlying momentum across sectors.

Given that monthly GDP averaged a ‑0.3% YoY contraction in January–February, today’s flash estimate implies that March activity rebounded to around 0.6% YoY. Our calculations suggest that economic activity in March was flat month over month, easing from +0.1% in February. The final GDP print and the March IGAE release are scheduled for May 22.

Our take: The data confirms that economic activity decelerated as expected in the first quarter, leaving a statistical carry‑over of -0.2% into 2026. This follows weakness in the annual growth in 1Q25, when recession concerns briefly emerged, but contrasts with the strong 4Q25 print, which mechanically boosted base effects. Recent March trade data suggest that exports contributed positively to 1Q growth, while IGAE indicators point to soft performance in services, agriculture, and mining. Looking ahead, near‑term momentum remains subdued, but we still anticipate a gradual recovery supported by firmer domestic demand and a modest boost from the 2026 FIFA World Cup, which we estimate will add 0.1pp to annual GDP growth. Even so, we revised our 2026 GDP growth forecast to 1.1%, down from 1.5% previously, reflecting weaker starting conditions.

See detailed data below