2026/05/22 | Julia Passabom & Mariana Ramirez

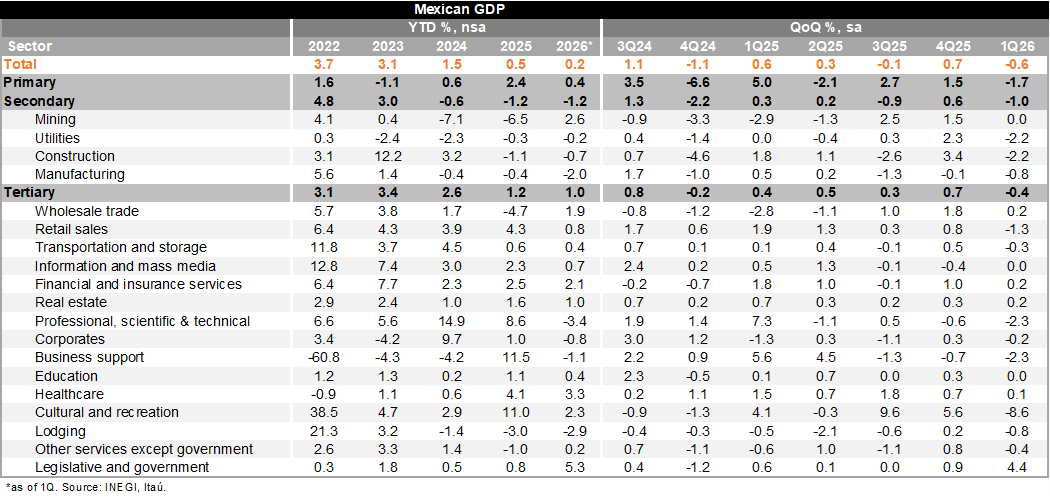

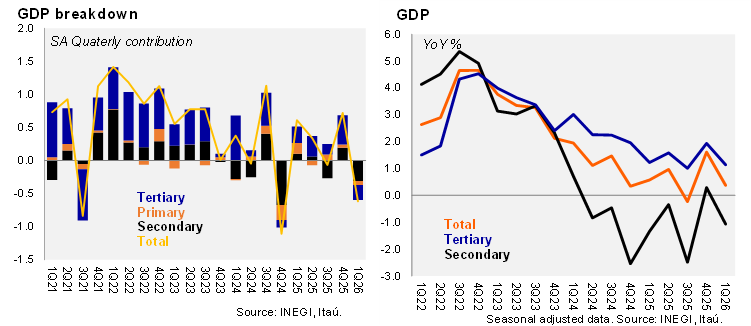

Final 1Q26 GDP expanded 0.2% YoY, modestly above the Bloomberg median, our forecast, and the flash estimate of 0.1%. By sector, primary activities rose 0.4% YoY (from -0.1% preliminary), industry contracted 1.2% YoY (vs. -1.3%), and services grew 1.0% YoY (vs. 0.7%). On a seasonally adjusted basis, GDP declined 0.6% QoQ, slightly better than the preliminary print (-0.8%) and closer to our forecast (-0.7%). The contraction was broad-based, with primary activities down 1.7%, industry -1.0%, and services -0.4%. Historical revisions were also incorporated, as we anticipated. GDP growth for 2024 was revised up to 1.5% (from 1.4%), while 2025 was revised down marginally to 0.5% (from 0.6%).

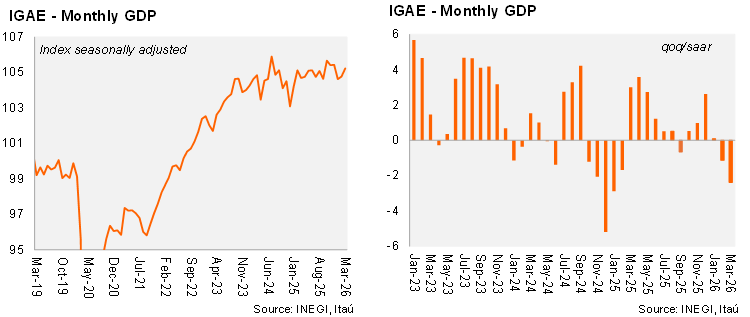

Monthly activity data (IGAE) surprised to the upside in March, rising 0.4% MoM (consensus: -0.02%, our forecast: -0.1%). Gains were driven by services (+0.8%) and agriculture (+4.5%), while industry declined 0.6%. Despite this rebound, momentum remains weak, with 1Q26 QoQ SAAR at -2.4%, deteriorating from -1.1% in the previous quarter.

Our take: The data confirm a loss of momentum following a strong 4Q25. Revisions improve the starting point for 2026, with statistical carry-over now at -0.03% (from -0.2%). While early 2Q indicators suggest some stabilization, near-term growth remains subdued. We continue to expect a gradual recovery supported by domestic demand and a modest boost from the 2026 FIFA World Cup (~0.1pp to GDP) and maintain our 2026 growth forecast at 1.1%.

See detailed data below