2026/04/02 | Julia Passabom, Mariana Ramirez &

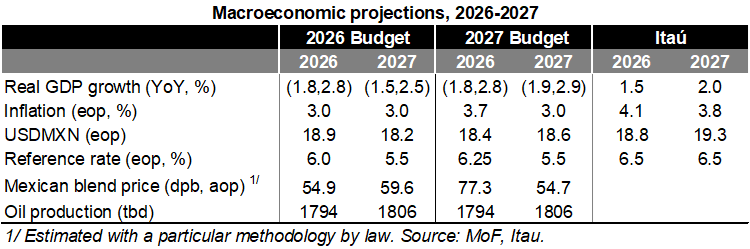

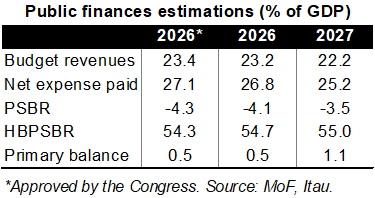

The Ministry of Finance (MoF) released the Preliminary Economic Policy Guidelines, updating the 2026 fiscal outlook and providing initial guidance for the 2027 Budget to be presented in September. The updated 2026 fiscal deficit projections show a modest improvement relative to the approved budget. The headline and primary balances are now estimated at -4.1% of GDP (from -4.3%) and 0.5% of GDP (unchanged), respectively. The narrower headline deficit reflects lower expenditures—primarily due to reduced allocations for Pemex debt amortization and a decline in interest costs (26.8% of GDP, down from 27.1%). Revenues were revised slightly lower to 23.2% of GDP (from 23.4%), driven by weaker Pemex-related income and the impact of gasoline subsidies. Meanwhile, the Historical Balance of Public Sector Borrowing Requirements (HBPSBR) was revised up to 54.7% of GDP (from 54.3%), largely reflecting INEGI’s upward revision to nominal GDP. Official 2026 GDP growth is foreseen at a range between 1.8-2.8%, above our call of 1.5% and Banxico’s analyst survey median (1.49%).

For 2027, the fiscal consolidation path remains broadly unchanged relative to prior guidance. The fiscal balance is projected at -3.5% of GDP, alongside a higher primary surplus of 1.1% of GDP (from 0.8%). However, the debt ratio is now expected to rise further to 55.0% of GDP (from 52.3%), pointing to a slower stabilization trajectory. The document also includes a preliminary list of priority spending programs for the upcoming budget, emphasizing social programs, migration-related services, multilateral engagement, R&D, and targeted support for women and indigenous communities. Official 2027 GDP growth is projected at a range between 1.9-2.9%; we forecast 2.0% and Banxico’s analyst survey median is at 1.82%.

Our View: The 2027 Pre-budget reinforces a continuity narrative rather than a policy shift, maintaining the medium-term framework of gradual fiscal consolidation following the 2024–2025 expansion. The strategy hinges on three key assumptions: (i) stable revenue growth, in the absence of a revenue-enhancing tax reform, (ii) expenditure discipline despite rising rigidities (notably pensions), and (iii) a supportive macroeconomic backdrop. Historically, Mexico has struggled to deliver on all three simultaneously, suggesting elevated execution risks.

The external environment has become more challenging. A potential escalation in the Middle East conflict introduces a dual channel via oil prices: while higher crude prices could boost oil revenues, they would likely reduce fuel tax (IEPS) collections through subsidy mechanisms, limiting net fiscal gains. For 2027, the government assumes an oil price of USD 54.7/bbl and updated its sensitivity analysis, estimating that each additional dollar per barrel generates MXN 9.6bn (~0.03% of GDP) in incremental revenues (down from MXN 11.6bn previously). Under our oil price assumption of USD 75/bbl, fiscal revenues could increase by approximately MXN 200bn (~0.6% of GDP).

At the same time, tighter global financial conditions could raise borrowing costs and complicate fiscal consolidation. Combined with persistent structural pressures—including Pemex support, rising pension liabilities, and infrastructure commitments—risks are skewed toward higher deficits. Our baseline assumes a terminal rate for Banxico at 6.5% (100bp above the assumption in the MoF’s projection), which could increase interest costs by roughly MXN 28bn in 2027. As a result, we continue to project a primary surplus of 0.7% of GDP, below the official target.

On the other hand, while the government’s 2026–2030 Infrastructure Investment Plan is referenced as a mechanism to close infrastructure gaps and boost productive capacity, it is not fully incorporated into the fiscal framework, nor are its growth contributions clearly quantified. Mexico’s historical experience suggests that large-scale infrastructure announcements alone have not translated into sustained growth. With a fiscal multiplier of approximately 0.6, the growth impact of public investment remains modest unless accompanied by: (i) high execution rates (above 80%, versus a historical range of 50%), (ii) sustained multi-year investment rather than front-loaded spending, and (iii) diversified project allocation. Against this backdrop, achieving the additional 2% of GDP in investment targeted for 2026 appears ambitious.

The final fiscal parameters for 2027 will be defined in the budget proposal to be submitted in September. While the consolidation framework remains intact, its credibility will depend on execution in an increasingly complex macro and financial environment.

See details below