2026/04/22 | Vittorio Peretti, Carolina Monzón, Juan Robayo & Angela Gonzalez

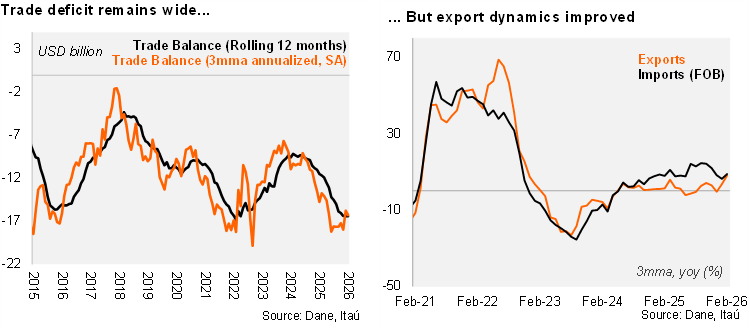

The trade deficit rose to USD 1.2 billion in February, unchanged from February 2025. The figure came in line with the Bloomberg market consensus, but below our USD 1.4 billion call. Total imports (FOB) increased by 8.5% YoY (+10.4% YoY in the previous month), driven by manufacturing imports, but partly contained by lower fuels and agriculture-related imports. Meanwhile, exports rose by 11.4% YoY (+12.8% in the previous month), although commodity exports remain weak. As a result, the 12‑month rolling trade deficit stands at USD 16.4 billion (USD 16.4 billion in 2025; USD 10.8 billion in 2024).

Internal demand continues to drive import growth. The 8.5% YoY increase was boosted by transport equipment (+39.7% YoY), durable consumption goods (+47.2% YoY), construction materials (+18.3% YoY) and non-durable consumption goods (+15.4% YoY), while partially contained by fuels (-18.2% YoY) and intermediate goods for agriculture (-10.5% YoY). In the rolling quarter ending in February, imports increased 8.8% (+8.2% in 4Q25). Imports excluding fuels and transport equipment rose by 11.2% from February last year. At the margin, we estimate imports increased 3.0% QoQ/saar (-3.3% in 4Q25). As of February, imports from the US accounted for 21.3% of total (23% in 2025).

Exports increased at the margin. Exports presented another double-digit expansion of 11.4% YoY (+12.8% YoY in January 2026). This outcome marks a rebound from the mild 1.3% YoY expansion set in 2025 and was driven by non-traditional exports, which grew at a pace of 28.2% (vs. 13.1% in overall 2025). During February, coal and coffee exports registered drops of 18.8% and 4.3% respectively, explained by both unfavorable price and volume effects. In contrast, oil exports expanded at a roughly 0.6% YoY pace amid an improvement in volumes. In the quarter ending February, exports increased 8.1% YoY (-0.4% in 4Q25). At the margin, we estimate exports grew by 12.1% QoQ/saar (-10.5% in 4Q25). As of February, exports to the US accounted for 31.5% of the total (29.6% in 2025).

Our Take: Imports remain supported by resilient domestic demand and exchange rate appreciation, while exports continue to face headwinds from weak commodity fundamentals although higher prices should provide some relief in months ahead. Accordingly, we forecast the current account deficit to increase from 2.4% of GDP in 2025 to 3.2% in 2026, albeit with downside risks from a narrower trade balance and weaker remittances.