2026/04/16 | Vittorio Peretti, Carolina Monzón, Juan Robayo & Angela Gonzalez

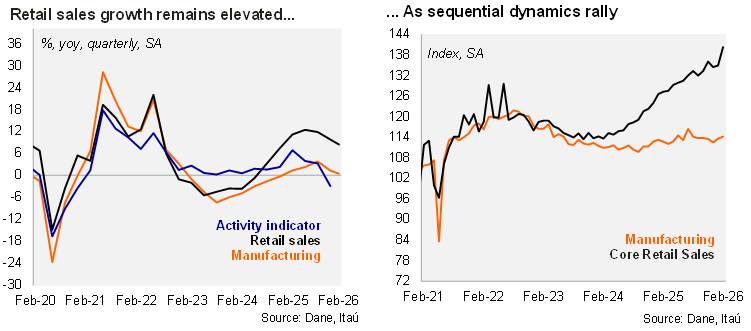

Activity indicators improved in February, lifted by retail. Retail sales rose by 10.9% YoY in real terms in February (+7.9% YoY in January), above both the Bloomberg market consensus and our 9.8% YoY forecast. Core retail sales (excluding fuels and vehicles) increased by 4.0% MoM/SA (+0.4% MoM/SA in the previous month), the swiftest pace since June 2022, resulting in a 10.7% real YoY increase (+8.8% YoY in January). Meanwhile, manufacturing output rose by 0.6% MoM/SA in February (+1.0% in January), leading to an annual increase of 1.4% YoY (0.3% YoY in January), overshooting the Bloomberg median of 0.2% and our 0% call.

Double‑digit growth in retail sales during the quarter. During the quarter ending in February, manufacturing increased by 0.1% YoY (+0.6% in 4Q25). At the margin, manufacturing dropped 1.0% QoQ/saar (-5.1% QoQ/saar in 4Q25). Retail sales rose by 10% YoY during the quarter ending February (+9.5% YoY in 4Q25), driven by vehicle and IT equipment sales. Sequentially, core retail sales increased 8.5% QoQ/saar (+6.7% QoQ/saar).

Our take: While manufacturing activity remains constrained, consumer demand continues to show resilience, underpinned by a tight labor market and the large real minimum wage adjustment. The February print of the coincident activity indicator (ISE) will be released on Monday. We expect a 2.1% YoY increase, supported by services and partly offset by weakness in mining and construction, though upside risks have increased following the stronger‑than‑expected activity data. With resilient consumer demand, and assuming the attendance of the finance minister in upcoming monetary policy decisions, our scenario considers a terminal rate of 12%, with a hike of 75 bps in the April 30 meeting.