2026/05/06 | Vittorio Peretti, Carolina Monzón, Juan Robayo & Angela Gonzalez

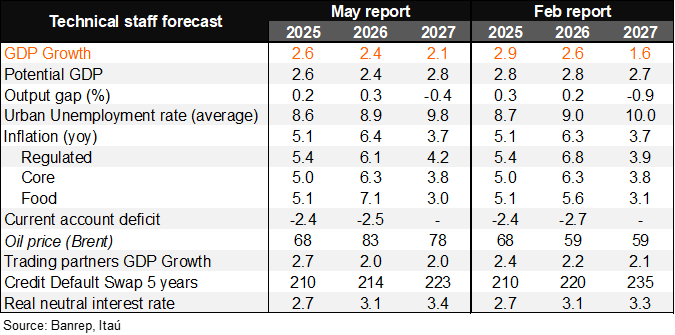

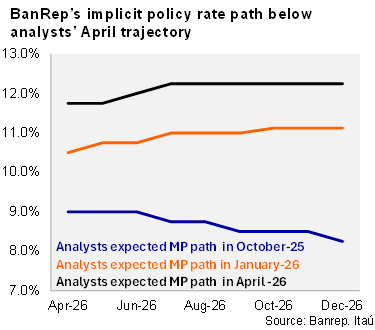

BanRep’s technical staff left inflation and neutral rate estimates broadly untouched in its quarterly Monetary Policy Report update. The 2026 year-end inflation forecast rose by 10 bps to 6.4% (Itaú: 7.0%; analysts: 6.3%; 5.1% in 2025), while the 3.7% for YE27 was retained (Itaú: 5.7%; analysts: 4.8%). The mild 2026 CPI upward revision incorporates higher food and input prices linked to the Middle East conflict and higher oil prices, temporary food supply disruptions in 2Q26 due to road blockades, larger‑than‑expected adjustments in utility tariffs, electronic shortages affecting tech goods prices, and stronger‑than‑anticipated wage increases. The forecast also incorporates the April gasoline price hike (COP 400 per gallon) and future gas tariff increases. These upside pressures are partly offset by disinflationary effects from the exchange rate, supported by more favorable terms of trade. Regarding monetary policy, the central bank staff’s baseline scenario implies a policy rate path that is, on average for 2026 and 2027, below analysts’ expectations of 12.25% in 4Q26 and 10.4% in 4Q27.

Food inflation revised up, offset by lower regulated prices. The core inflation forecast for YE26 remained unchanged at 6.3%, well above the 2–4% target range, while the YE27 forecast is still seen at 3.7%. Regulated CPI was revised down by 70 bps to 6.1% in 2026 and is expected to ease to 4.2% in 2027 (+30 bps vs. the previous report), reflecting downside surprises in gasoline prices and utility price adjustments in 1Q26. Food inflation is now expected to close 2026 at 7.1% (from 5.6%), before reverting to 3.0% by YE27 (3.1% previously), driven by supply‑side pressures in perishables amid La Niña, stronger meat demand, and temporary disruptions, with upside risks tied to climate uncertainty, global food and fertilizer prices, and a higher probability of El Niño in 2H26.

Despite lingering inflation pressures, the signaled interest rate path implies the cycle is nearing its conclusion. The staff maintained their real neutral rate estimate at 3.1% for 2026, while raised the 2027 estimate by 10bps to 3.4%. On the external front, BanRep’s technical staff assumes the Fed will stay on hold in 2026 (two cuts previously expected), with only one cut in 2027. Regarding monetary policy, the central bank staff’s baseline scenario implies a policy rate path that is, on average for 2026 and 2027, below analysts’ expectations for the MPR of 12.25% in 4Q26 and 10.4% in 4Q27.

The output gap will remain positive in 2026, amid resilient domestic demand. GDP growth for 2026 was revised down by 0.2pp to 2.4%, reflecting negative, mostly supply‑side shocks and statistical revisions, while the 2027 forecast was revised up by 0.5pp to 2.1%. Domestic demand continues to expand, supported by public consumption, although private consumption growth has moderated and investment remains constrained by weak construction activity. The output gap remained broadly stable at +0.3% in 2026 but is seen turning negative in 2027 to -0.4% (vs. -0.9% expected in the previous report).

Our Take: While the Board kept the policy rate unchanged, central bank staff flagged upside inflation risks. The Middle East conflict and the potential materialization of El Niño could push energy prices even higher. We expect BanRep to resume the hiking cycle at the June meeting, with the policy rate reaching 12.50% by year‑end. The minutes of the last meeting will be released later today.