2026/02/13 | Vittorio Peretti, Carolina Monzón, Juan Robayo & Angela Gonzalez

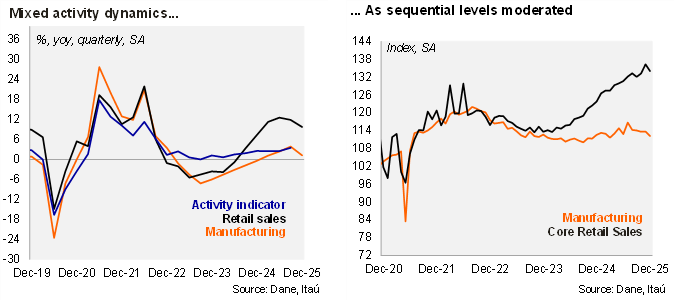

Strong retail dynamics contrast with weak manufacturing.Retail sales rose by 11% YoY in real terms in December (+7.5% YoY in November), above the Bloomberg median of 8.9% YoY and our 8.0% call. Core retail sales (excluding fuels and vehicles) fell by 1.7% MoM/SA (+2.3% in the previous month), leading to an 8.6% YoY rise in real terms (+11.8% YoY in the previous month). However, manufacturing fell sequentially by 1.3% MoM/SA (unchanged in November), resulting in a 0.6% YoY contraction (+0.7% in the previous month), below the Bloomberg median of +1.2% and our +1.5% call.

The pace of sequential retail sales growth remains elevated, but is gradually slowing. During the final quarter of the year, manufacturing increased by 0.7% YoY (+4.1% rise in 3Q25). At the margin, manufacturing dropped 6.2% QoQ/saar (down from +5.2% in 3Q25). Retail sales rose 9.6% YoY in the 4Q25 (+15.2% in 3Q25), while core retail sales increased 10.1% YoY (+12.9% in 3Q25), driven by vehicles and IT equipment. Sequentially, core retail sales increased 6.2% QoQ/saar (from +8.2% QoQ/saar in 3Q25).

Our Take: Despite softer manufacturing, domestic demand remains strong amid a tight labor market. For the 4Q25 GDP release on February 16, we foresee the economy to have grown by 2.8% in 2025, boosted by household and public consumption. Nevertheless, we forecast a deceleration of activity to 2.3% in 2026, amid higher interest rates after the sharp minimum wage increase. Alongside the publication of the national accounts, the monthly coincident indicator (ISE) for December will be released. We expect an increase of 1.2% YoY, boosted by tertiary sectors, but dragged by mining and construction.