2026/03/16 | Vittorio Peretti, Carolina Monzón, Juan Robayo & Angela Gonzalez

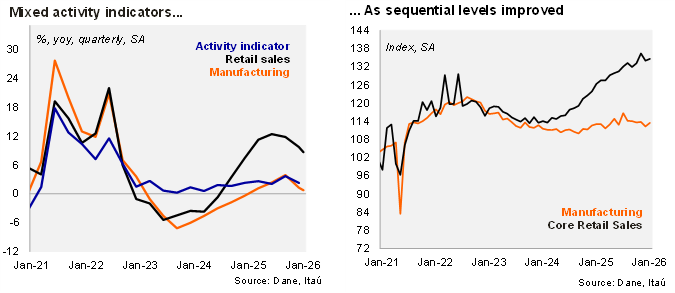

Retail sales growth remained elevated in January. Retail sales rose by 7.8% YoY in real terms in January (+11% YoY in December), below the Bloomberg market consensus of 10% YoY and our 10.9% forecast. Core retail sales (excluding fuels and vehicles) increased by 0.4% MoM/SA (-1.8% MoM/SA in the previous month), leading to an 8.8% annual real rise (+8.6% in December). Meanwhile, manufacturing output rose by 1.1% MoM/SA in January (-1.3% in December), consistent with an annual contraction of 0.5% YoY (-0.6% in December), undershooting the Bloomberg median and our +0.5% call.

Manufacturing remains a drag on growth. Over the quarter ending in January, manufacturing declined by 0.1% YoY (+0.6% in 4Q25), and contracted by 2.6% QoQ/saar. Retail sales rose by 8.9% YoY during the January quarter (+9.5% YoY in 4Q25), while core retail sales increased by 9.6% YoY (+10% YoY in 4Q25), driven by stronger vehicle and IT equipment sales. Sequentially, core retail sales expanded by 6.9% QoQ/saar, up from 6.5% QoQ/saar in 4Q25.

Our Take: Despite weak manufacturing, consumption remains resilient, supported by a tight labor market. The January reading of the monthly coincident indicator (ISE) will be published on Wednesday. We project a 2.7% year-over-year increase, led by services and partially offset by weakness in mining and construction, although risks are tilted to the downside following today’s surprise in activity indicators.