2026/04/10 | Vittorio Peretti, Carolina Monzón, Juan Robayo & Angela Gonzalez

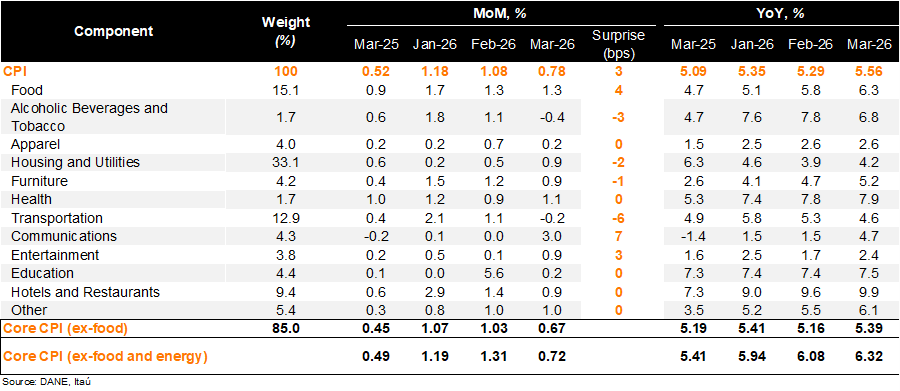

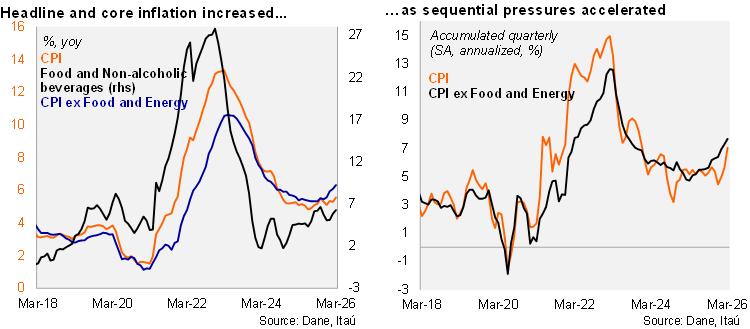

Headline and core inflation rebounded in March, surprising the market to the upside. Consumer prices rose by 0.78% MoM (+1.08% in February), above the Bloomberg market consensus of 0.69%, while closer to our 0.75% call. The main positive contributors in the month were housing and utilities (+0.85% MoM; +26bps), food (+1.27% MoM; +24bps) and hotels and restaurants (+0.89% MoM; +10bps). Consumer prices excluding food rose by 0.67% MoM (+0.45% one year earlier), while inflation excluding food and energy increased by 0.72% MoM (+0.49% MoM one year earlier). On an annual basis, headline inflation increased by 27bps from February to 5.56%, while core inflation increased by 24bps to 6.32%, the highest level since July 2024. Services inflation continued to rise, moving well above 7% year over year.

Amid high services inflation, core dynamics accelerated at the margin. Non-durable goods inflation (mainly food) came in at 3.92% YoY (+27bps from the previous month). Meanwhile, energy inflation remained in negative territory, but eased 11bps to -2.6% YoY. With the COP remaining at favorable levels, durable goods inflation fell by 4bps to 0.7% YoY. Services inflation rose by 32bps to 7.3% YoY (9.51% peak in September 2023), reflecting indexation effects following the minimum wage hike. At the margin, we estimate that inflation accumulated in the quarter was 7.1% (SA, annualized; 4.5% in 4Q24). Core inflation rose to 7.7% from 6.4% in 4Q24 (SA annualized).

Our take: Our preliminary estimate for April’s monthly inflation, scheduled for release on May 8, ranges between 0.65% and 0.75%, resulting in the annual CPI print between 5.6% and 5.7%. Additionally, the downward impact from fuel prices observed in February and March will no longer be present in April, following the upward adjustment in fuel prices, which is expected to contribute 7 bps to April’s inflation print. Our baseline scenario puts the YE26 inflation at 6.7% (analyst survey & BanRep’s staff: 6.3%). With this inflation outlook, and assuming the attendance of the finance minister in upcoming monetary policy decisions, our scenario considers a terminal rate of 12%, with a hike of 75 bps in the April 30 meeting.