2026/02/18 | Vittorio Peretti, Carolina Monzón, Juan Robayo & Angela Gonzalez

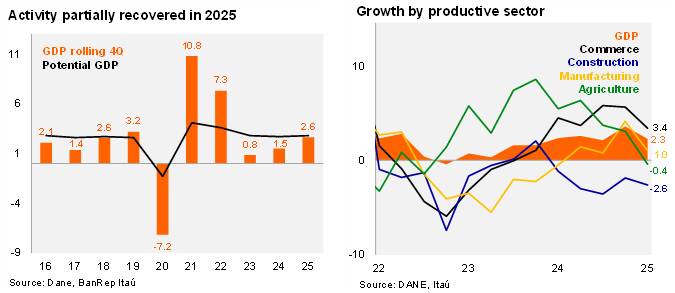

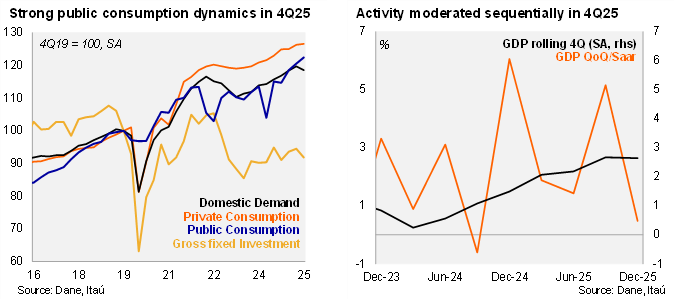

The Colombian economy grew by 2.6% in 2025 (1.5% in 2024), below BanRep’s 2.9% forecast and our 2.8% call. The weaker print came as growth slowed to 2.3% YoY in 4Q25 (+3.6% in 3Q25), below the Bloomberg median (2.8%) and BanRep technical staff’s 3.0%, while closer to our 2.5% call. On the supply side, the annual increase was driven by public administration (+4.8% YoY; +0.9pp), commerce (+3.4% YoY; +0.7pp), and entertainment (+11.5% YoY; +0.5pp), but constrained by declines in mining (-2.9% YoY; -0.1pp), construction (-2.6% YoY; -0.1pp), and IT sectors (-1.2% YoY; -0.04pp). On the demand side, growth was supported by public and private consumption, while gross fixed investment contracted. Sequentially, the economy increased a mild 0.1% (SA) from 3Q25 to 4Q25 (+1.3% in 3Q25).

Public consumption remains a growth driver, but investment is weak. Gross fixed investment fell by 2.9% YoY in the quarter (BanRep technical staff’s: +3.2% SA), due to a contraction in housing investment (-8.5% YoY in 4Q25), but partially contained by a moderate increase in machinery and equipment. Total consumption increased by 3.8% YoY (+5.7% in 3Q25), lifted by public consumption rise of 5.9% (BanRep technical staff’s: +5.8% SA), while private consumption rose 3.1% (BanRep technical staff’s: +4.3% SA). Exports increased 1.2% over one year (+2.7% in 3Q25), while imports dynamics moderated despite exchange rate appreciation, increasing by 1.4% YoY (+9.9% in 3Q25). On the supply side, the natural resource sector dropped 1.3% YoY (-0.15% in 3Q25). Non-natural resource activity increased by 2.7% (4.0% in 3Q25).

At the margin, activity increased 0.5% QoQ/saar, down from the +5.2% registered in 3Q25. The seasonal and calendar adjusted series shows that gross fixed investment dropped at a double-digit rate. Private consumption grew at a limited rate of 1.0% QoQ/saar.

The coincident activity indicator (ISE) expanded 0.9% from November to December (SA, -1.2% MoM in November). On an annual basis, the ISE posted an expansion of 1.7% YoY in December, below the Bloomberg median (2.6%), but higher than our 1.2% call.

Our Take: Although the services sector remains robust, driven by public expenditure, some key productive sectors, such as construction and mining, remain in deep in negative territory. We expect the economy to grow by 2.3% in 2026 (2.6% in 2025). Contractionary monetary policy should slow private consumption, while business dynamics are likely to keep investment downbeat.