2026/05/15 | Vittorio Peretti, Carolina Monzón, Juan Robayo & Angela Gonzalez

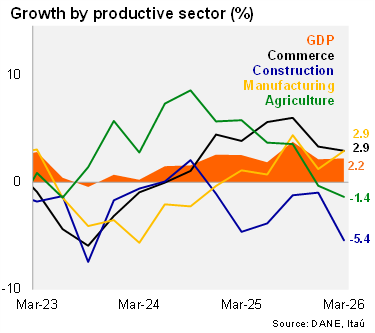

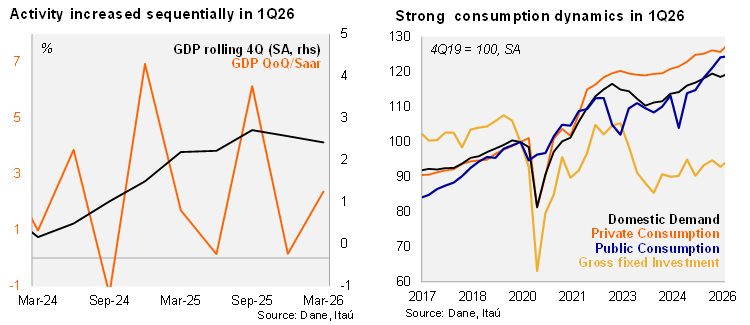

Economic activity increased by 2.2% YoY in 1Q26 (+2.1% in 4Q25; revised down by 0.2 pp), above the BanRep staff’s 2.1% forecast, the Bloomberg consensus, and our 2.0% estimate. In annual terms, activity was driven by public administration (+5.7% YoY; +0.9 pp), commerce (+2.9% YoY; +0.6 pp), and real estate (+2.0% YoY; +0.2 pp). Construction (‑5.4% YoY; ‑0.3 pp) and agriculture (‑1.4% YoY; ‑0.2 pp) offset the upbeat dynamics. Sequentially, the economy expanded by 0.6% QoQ/SA from 4Q25 to 1Q26 (flat in 4Q25), mainly supported by gross fixed investment and both public and private consumption.

Gross fixed investment keeps recovering, while housing contracts again. Gross fixed investment rose by 3.7% YoY (-2.0% YoY in 4Q25), due to an increase in machinery and equipment (+12.8% YoY), but dragged by housing (-3.2% YoY). Total consumption increased by 3.4% YoY (+3.9% YoY in 4Q25), lifted by public consumption (+7.8% YoY; +9.2% in 4Q25) and private consumption (+2.7% YoY; +2.3% in 4Q25). Thus, domestic demand grew 2.3% YoY (+2.1% in 4Q25). Exports increased by 3.5% over one year (+3.7% in 4Q25), while imports rose by 3.5% YoY (+2.9% in 4Q25). On the supply side, natural resource sector rose 2.6% YoY (+2.5% in 4Q25), lifted by the mining sector.

At the margin, activity increased by 2.4% QoQ/saar. The seasonal and calendar adjusted series show that gross fixed investment increased 8.4% QoQ/saar (-7.7% in the previous quarter), lifted by machinery and equipment, while private consumption rose by 8.0% QoQ/saar (-1.5% in 4Q25) and public consumption +1.1% QoQ/saar (+10.5% in the 4Q25). Imports posted more momentum in the quarter, while exports decelerated.

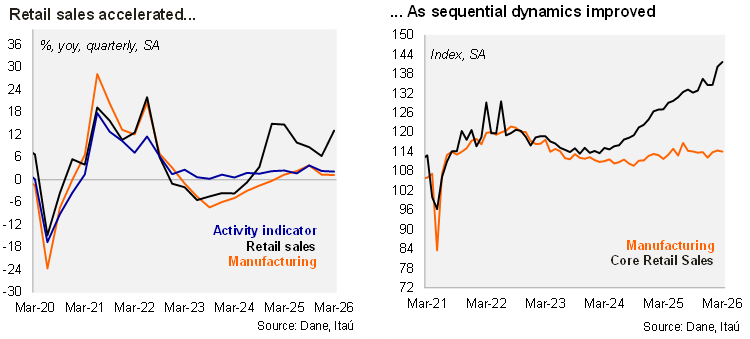

The coincident activity indicator (ISE) posted a 4.0% YoY increase (2.2% MoM/SA) in March. The outcome was supported by tertiary activities such as commerce and financial services, highlighting the strength of private consumption and the presence of inflationary pressures. During the month retail sales rose by 13.4% YoY in real terms in March (+11% YoY in February), above both the Bloomberg market consensus and our forecast (9.9% and 8.3%, respectively). Similarly, manufacturing posted a 3.9% YoY expansion (1.3% YoY in February), overshooting the Bloomberg median of 1.4% and our 3.0% call. Sequentially, manufacturing production fell by 0.3% MoM/SA, partially reversing the 0.5% MoM/SA expansion in the previous month.

Our Take: Economic activity continues to be driven primarily by public and private consumption. Consumer demand continues to be resilient, underpinned by a tight labor market and a significant real minimum wage adjustment. In an environment of elevated interest rates and high inflation, the momentum of domestic demand is likely to moderate. As a result, we expect activity to grow by 2.1% this year (+2.6% in 2025; +1.5% in 2024). Given the resilience of economic activity and domestic demand, we expect BanRep to resume the monetary policy tightening cycle as early as June.