2026/03/12 | Vittorio Peretti, Carolina Monzón, Juan Robayo & Angela Gonzalez

Lower primary spending and interest payments drive the fiscal adjustment. The lower projected 2026 fiscal deficit is underpinned by a reduction in total expenditure to 21.2% of GDP, well below the previous official forecast (24.4%; 22.7% in 2025). Primary spending would see the largest adjustment, falling by 1.4pp to 18.2% of GDP in the previous official forecast (19.9% in 2025), while interest payments would reach 3.0% of GDP (2.8% in 2025). However, projected total revenues were revised down by 2.1pp to 16.1% of GDP (16.3% in 2025), mainly due to lower tax revenues.

The primary balance forecast of -2.1% of GDP is based on a net structural primary balance (NSPB) of -1.2% of GDP, which could be increased by 0.2pp and 0.7pp due to economic and oil cycles, respectively. It is worth noting that the government applied the fiscal rule escape clause in June 2025, implying that the technical gap parameters are not followed.

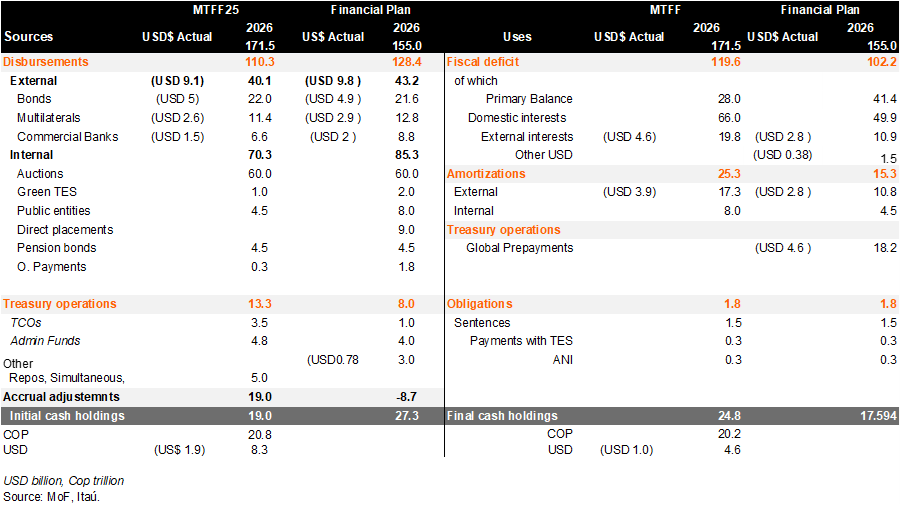

The central government’s gross financing needs are estimated at COP 102.2 trillion (5.1% of GDP). The 2026 financing strategy considers 66% local currency and 34% foreign currency (compared to the 63%/36% indicated in the MTFF). The total deficit is planned to be financed with COP43 trillion (USD9.8 billion) of external issuances, of which COP 21 trillion will be global bonds (USD 4.9 billion) already issued in early January. In February, the Public Credit Director mentioned that 29% of external financing was expected through multilateral loans (USD 2.9 billion), while the remainder of USD 2.6 billion is to be raised through commercial loans with foreign banks (USD 4.3 billion in 2025).

Closure of the TRS and bond prepayment are key priorities. In previous statements, the MoF referred to treasury operations for COP18.1 trillion in global pre-payments (USD4.7 billion) which account for 17.7% of the overall deficit. Moreover, the Public Credit Director remarked that the USD 9.3bn TRS operation will be fully repaid before the end of the administration.

Cash is king. In 2026 the MoF will continue to strengthen its cash position. After ending 2025 at COP 27.3 trillion, by February the MoF reported balances of COP 6.6 trillion in local currency and USD 10billion in foreign currency. Altogether, the MoF targets final cash holdings of COP 17.6 trillion.

Our take: Achieving the proposed fiscal consolidation requires significant spending efforts. While the recent spike in oil prices could provide some fiscal relief, if gasoline and diesel subsidies remain in place, the impact would likely be limited. For 2026, we forecast a nominal fiscal deficit of 7.4% of GDP and a likely return of net debt above the 60% threshold.