2026/04/30 | Vittorio Peretti, Carolina Monzón, Juan Robayo & Angela Gonzalez

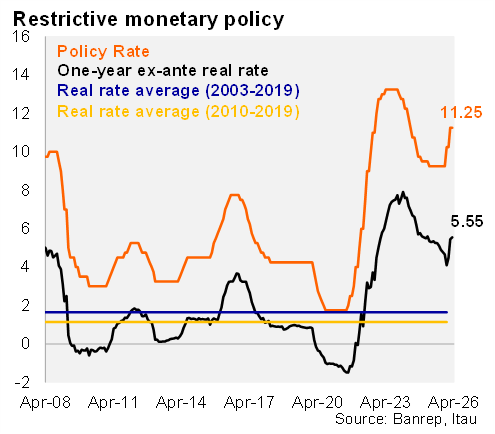

BanRep’s board holds the policy rate at 11.25%, after the 100 bp hikes delivered at the January and March meetings. The decision came well below the Bloomberg median of 11.75%, and our 12% call. Despite institutional tensions, the MoF attended the Board meeting. After seven meetings with split decisions, the Board reached a unanimous vote again. Following the decision, the one-year ex-ante real interest rate rose slightly to 5.5%, up from 5.4% after March’s meeting and well above BanRep’s estimated neutral real rate of 3.1% for 2026, underscoring the highly restrictive policy stance. Governor Villar remarked that board members continue to hold differing views but agreed to keep rates unchanged in an effort to build consensus under the current conditions.

Governor Villar stated that the hiking cycle has not yet been concluded. Villar noted that the message from the last two meetings has been the need to act preemptively and adjust rates swiftly to gain flexibility. The group that voted for hikes in previous meetings does not rule out further increases, although Villar emphasized that the policy rate is already in contractionary territory. Villar noted that the technical staff put forward a strictly technical recommendation, which the governor chose not to elaborate on during the press conference to avoid potential confusion, as it did not incorporate current sources of uncertainty on either the external or domestic fronts, amid tensions between the Central Bank and the government.

Inflation developments will determine the need for further rate adjustments. Governor Villar highlighted that inflation rose to 5.6% in March, up 46 bp from December, while core inflation reached 5.8%, 80 bp above end‑2025 levels. Meanwhile, 12‑month inflation expectations declined, but year‑end expectations ticked up again. Moreover, amid higher oil prices, the MoF announced a COP 400 increase (3% MoM) in fuel prices in May, marking the second consecutive month of upward adjustments, contributing 9bps to monthly inflation (+8bps estimated for April).

Activity growth remains resilient. Activity indicators point to 1Q26 growth exceeding that of 4Q25, while the labor market remains dynamic, with historically low unemployment and a rising share of salaried employment.

External uncertainty remains elevated. A prolonged Middle East conflict could generate additional upward pressures on energy and fertilizer prices and lead to tighter external financial conditions.

Our take: Despite the decision to keep the policy rate unchanged at 11.25%, amid institutional tensions, inflation and inflation expectations remain well above target from; risks remain skewed to the upside amid heightened geopolitical uncertainty and a higher likelihood of an El Niño event. With headline and core CPI inflation rebounding and domestic demand still strong, we still see room for the Board to deliver further hikes ahead. Therefore, we do not see this as the end of the tightening cycle. May holds a non monetary policy decision. On Tuesday, the central bank will publish its monetary policy report for 1Q26 and on Wednesday, the minutes of April’s monetary policy meeting will be released.