2026/06/30 | Vittorio Peretti, Carolina Monzón, Juan Robayo & Angela Gonzalez

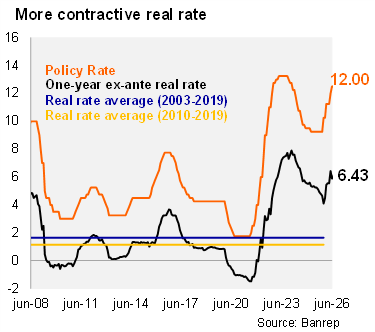

BanRep raised the policy rate by 75bps to 12%, in line with our call, but above the Bloomberg median of a 50bps hike. Following April’s unexpected pause—seen as an effort to insulate BanRep from the electoral cycle—the Board has resumed its tightening path. As expected, the decision reiterated the division in the Board: four members supported a 75bp hike, two favored a 50bp increase, and one voted to hold. In real terms, the one‑year ex‑ante policy rate rose to 6.4%, up from 5.5% after the April meeting and well above the Bank’s estimated neutral rate of 3.1% for 2026, highlighting the clearly restrictive stance. Governor Villar noted that both headline (5.8%) and core inflation (6.0%) continue to trend upward, remaining significantly above target. Inflation expectations, while falling since June, remain volatile and above 3% across all horizons.

On the activity side, momentum remains firm, supported by robust domestic demand. Economic growth reached 2.2% in 1Q26, while the labor market continues to show strength, with unemployment at historically low levels and ongoing wage gains.

Villar emphasized that while tight labor market conditions can generate inflationary pressures, inflation dynamics hinge critically on the credibility of the central bank. Even in a context of low unemployment, inflation can converge to target if policy credibility is preserved. Sustaining low unemployment while ensuring disinflation, therefore, depends on maintaining confidence in the inflation‑targeting framework.

Looking ahead, the Board signaled that further rate hikes remain on the table, with decisions fully data‑dependent. Villar reiterated that it is too early to determine how close the cycle is to its end, with current policy settings aimed at guiding inflation back toward target. Staff projections see inflation closing 2027 at around 4%, with convergence to the 3% target only by 2028. Near‑term risks remain tilted to the upside. Adverse weather conditions could exert additional pressure on food prices toward year‑end, while regulated prices warrant monitoring. On the positive side, lower oil and fertilizer prices offer some external relief. For now, the Ministry of Finance has kept gasoline and diesel prices unchanged for July.

Our take: Despite recent currency strength, a combination of resilient demand, a tight labor market, elevated inflation, and persistently high expectations continues to skew risks to the upside. With additional climate‑related pressures likely in 2H26, we expect BanRep to continue tightening, reaching a terminal rate of 13% by year‑end. The next monetary policy meeting is scheduled for July 31.